Oil and gas sector of the economy Russian Federation is the basis for the formation of the country's budget. At the end of 2014, receipts from oil and gas industry amounted to 6 813 billion rubles. This is 48% of all federal budget revenues. The value of the Russian currency largely depends on world prices. The oil and gas industry in Russia consists of three main sectors: production, transportation and processing of oil and gas.

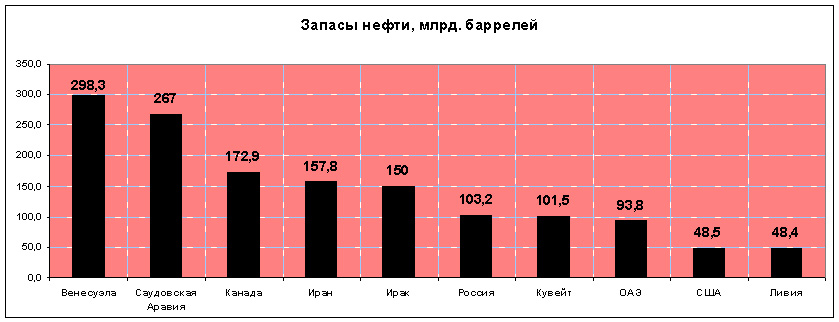

Proved in Russia according to data for 2014 is about 103.2 billion barrels. This is the sixth largest in the world. Proved reserves mean the amount of minerals that can be extracted using modern technologies. Venezuela is the leader in terms of the amount of oil reserves - 298.35 billion barrels. But many experts are inclined to think that since oil is a strategic raw material, some countries may deliberately underestimate or overestimate their own reserves.

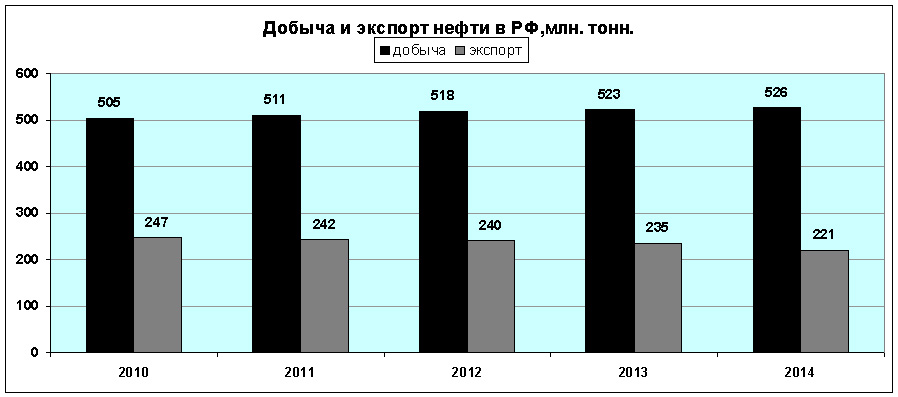

As for oil production in the Russian Federation, at the end of 2014, 526 million tons were extracted. Of these, 221 million tons were exported, which is 42% of the total oil production. Compared to 2013, oil production increased by 0.5%, while exports decreased by 6%.

The Russian Federation ranks first in the world in terms of proven reserves of natural gas. Russia has 47.6 trillion. cubic meters of gas. This represents 32% of all world reserves. After Russia, the most important suppliers of "blue fuel" are the countries of the Middle East.

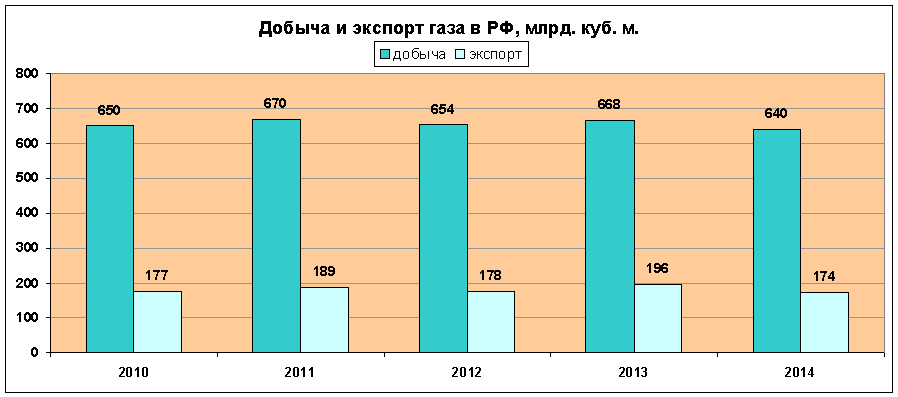

By the end of 2014, 640 billion cubic meters were produced in Russia. meters of natural gas. Compared to 2013, production fell by 4.2%. Exported was sent 27.1% of all production, which is equivalent to 174 billion cubic meters. m. of fuel.

The total value of the volume of crude oil exports from the Russian Federation in 2014 amounted to 153.88 billion US dollars, the value of export natural gas - 55.24 billion US dollars.

To transport oil and gas in Russia, a network of trunk pipelines was built, which in 2014 totaled about 260 thousand km. Of these, the share of oil pipelines is about 80 thousand km, the share of gas pipelines is 165 thousand km, about 15 thousand km is the share of oil product pipelines. In terms of the length of pipelines, Russia is in second place in the world, lagging behind the leader, the United States, by almost 10 times. The third place is taken by Canada, with a total length of pipelines of about 100 thousand km.

At the beginning of 2014, oil production in Russia was carried out by 294 companies that have the relevant permits. 111 of them are vertically integrated companies (vertically integrated companies), that is, they carry out several -processes in this industry (production, transportation, processing, sale of oil and oil products). 180 independent companies not included in the structure of vertically integrated oil companies and 3 companies operating under a production sharing agreement (PSA). A PSA is a specific agreement concluded between the mining company (contractor) and the state. Under this agreement, the contractor is entitled to carry out prospecting and exploration and geological work, as well as to exploit mineral deposits in a certain area.

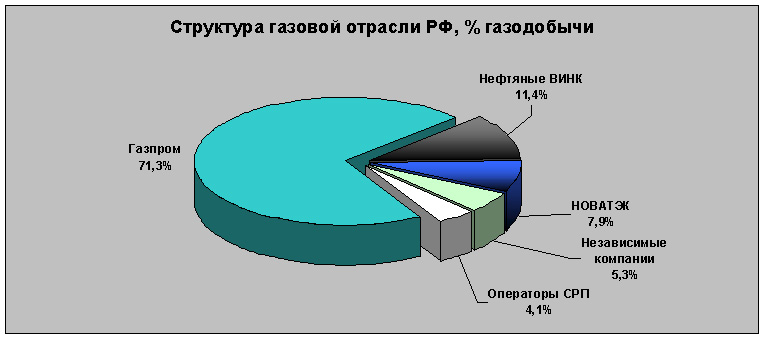

There were 258 companies in the gas industry in 2014. Of these, 97 companies were part of the structure of oil vertically integrated oil companies, 16 - into the structure of Gazprom, 2 - into the structure of NOVATEK, and 140 are independent companies. There are 3 companies operating under the PSA agreement.

Oil and gas workers in the Russian Federation receive the highest wages in the country. It is quite problematic to calculate the average salary in the industry, since the difference between the salaries of different employees is very large. Workers with the lowest qualifications, on average, receive 60 - 80 thousand rubles per month, qualified personnel about 150 - 180 thousand rubles, and the salaries of managers can reach 300 - 400 thousand rubles and more.

Oil and gas fields in the Russian Federation

The largest oil and gas region of the Russian Federation is Western Siberia. Here, in the Yamalo-Nenets and Khanty-Mansi Autonomous Okrugs, a significant part of natural gas and oil is produced. Oil production by regions of the Russian Federation is as follows:

- Western Siberia - 60%

- Ural and Volga region - 22%

- Eastern Siberia - 12%

- North - 5%

- North Caucasus - 1%

As for the production of natural gas, the share Western Siberia here it is even higher than in oil production:

- Western Siberia - 87.3%

- Far East - 4.3%

- Ural and Volga region - 3.5%

- Eastern Siberia and Yakutia - 2.8%

- North Caucasus - 2.1%

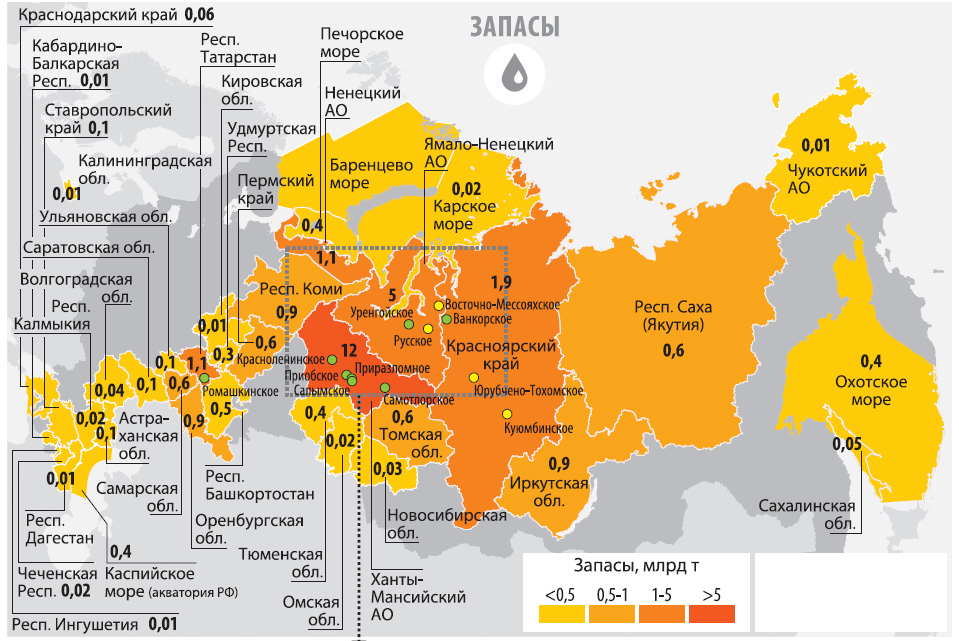

A total of 2,352 oil fields are being developed in Russia. Of these, 12 are unique and 83 are large. Of the 12 unique deposits, 5 are located in the Khanty-Mansi Autonomous Okrug, 3 in the Krasnoyarsk Territory, 3 in the Yamalo-Nenets Autonomous District and 1 in the Republic of Tatarstan.

The largest field in Russia is Samotlorskoye, with estimated oil reserves of 7.1 billion tons. Average daily production is about 65 thousand tons. The deposit is located in the Khanty-Mansi Autonomous Okrug. The development is carried out by the oil company Rosneft.

The largest oil field in Russia in terms of average daily production is Priobskoye. The field is also located in the Khanty-Mansiysk Autonomous District and produces about 110 thousand tons of oil daily. The explored reserves amount to about 5 billion tons of oil, the production is carried out by the companies "Rosneft", "", "Sibneft - Yugra".

Prirazlomnoye, Krasnoleninskoye and Salymskoye are 3 more fields of the Khanty-Mansi Autonomous Okrug, which are among the unique oil fields in Russia. Explored oil reserves are 0.4, 1.1 and 0.5 billion tons. Average oil production per day for Prirazlomnoye field is 20.5 thousand tons, at Krasnoleninskoye - 21.7 thousand tons, at Salym - 2.2 thousand tons. Six oil companies are producing at the Krasnoleninskoye field, while the Prirazlomnoye and Salymskoye fields are developed by Rosneft.

In addition to 5 unique oil fields there are 2 fields in the Khanty-Mansiysk Autonomous Okrug, which are among the five largest in Russia in terms of total oil reserves - Lyantorskoye and Fedorovskoye. The initial stocks of raw materials here amounted to 2 and 1.8 billion tons, respectively. But since the fields have been developed since the 70s of the last century, residual oil reserves at the Lyantorskoye field are about 320 million tons, and at Fedorovskoye - about 150 million tons. The average daily productivity of the Liaontorskoye field is 26 thousand tons, Fedorovskoye - 23 thousand tons.

Romashkinskoye is the largest oil field in the Urals and the Volga region and the European part of Russia as a whole. It is located in the Republic of Tatarstan, and the total geological reserves of oil here are about 5 billion tons. Over the years of operation, about 3 billion of oil have been extracted from the field. Now the average daily production is about 41 thousand tons. The field is being developed by the Tatneft company.

2 unique fields in the Yamal-Nenets Okrug belong to the category of developed ones, one - Urengoyskoye, is the largest gas field in the country. The level of oil production at the Urengoyskoye field is about 1,000 tons per day. The Russkoye and Vostochno-Messoyakhskoye deposits are one of the most promising in the Russian Federation; the total geological reserves of these deposits amount to about 2 billion tons. Development should begin in 2015-16.

The Vankor oil field is the largest in the Krasnoyarsk Territory. About 50.5 thousand tons of oil are produced here per day, and the reserves are about 450 million tons of oil. The remaining 2 fields of the Krasnoyarsk Territory - Yurubcheno-Takhomskoye and Kuyumbinskoye are small, their reserves amount to about 250 million tons of oil.

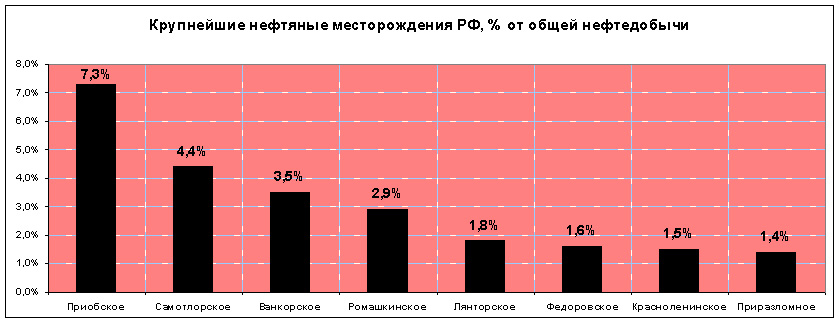

The structure of oil production in Russia is such that the 8 largest fields provide about 25% of the oil produced.

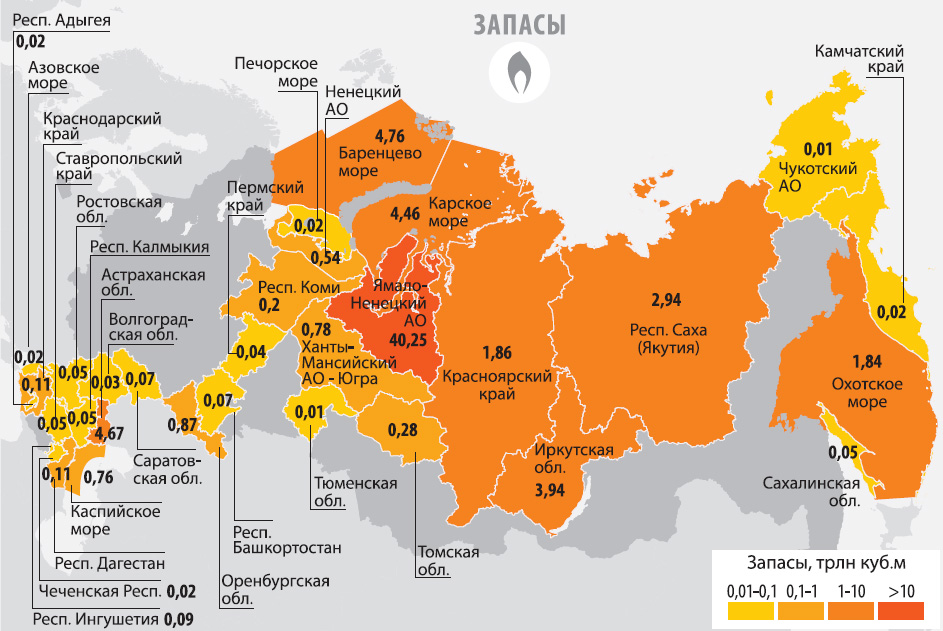

Gas production in Russia is concentrated mainly in the Yamalo-Nenets Autonomous District. About 81% of Russian natural gas is produced here. This Autonomous Okrug contains 8 of the 10 largest Russian gas fields by the amount of recoverable fuel.

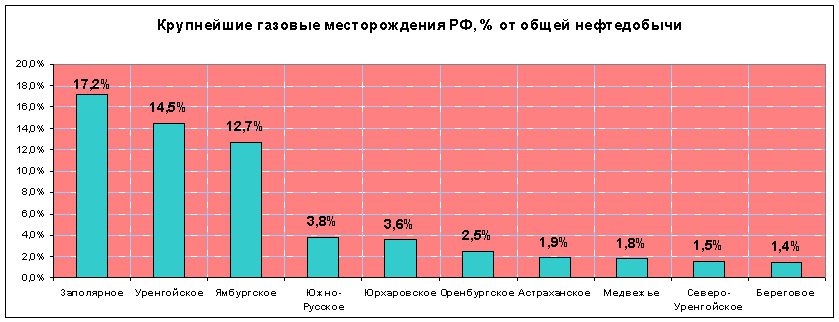

The Urengoyskoye field is the largest in Russia and the second largest in the world in total natural gas reserves. The total reserves of blue fuel here are about 10 trillion. cub. m. Average annual production is 95.1 billion cubic meters. m.

In terms of the amount of recoverable natural gas in the Russian Federation, the leader is the Zapolyarnoye field. Here, the average annual production is equal to 112.6 billion cubic meters. m. The number of general reserves is about 3.5 trillion. cub. m.

The second largest gas reserves in the Russian Federation is the Yamburgskoye field. The total geological reserves are estimated at 5.2 trillion. cub. m. In terms of average annual production, this field ranks third in Russia - 83.6 billion cubic meters. m.

In addition to the above, 5 more fields in the Russian top ten are represented by the Yamalo-Nenets Autonomous District.

- Yuzhno-Russkoye - average annual production of 25.3 billion cubic meters. m.

- Yurkharovskoye - average annual production of 23.9 billion cubic meters. m.

- Bearish - average annual production of 12.2 billion cubic meters. m.

- Severo-Urengoyskoye - average annual production of 10 billion cubic meters. m.

- Beregovoye - average annual production of 9.5 billion cubic meters. m.

In other regions of the country, there is the Orenburg field, which represents the Volga-Ural oil and gas basin and the Astrakhan (Caspian oil and gas basin). The average annual production of natural gas in the Orenburgskoye field is 16.4 billion cubic meters. m., in Astrakhan - 12.8 billion cubic meters. m.

In contrast to oil production, the 10 largest gas fields account for a significant share of recoverable "blue fuel" - more than 61%. Moreover, about 45% falls on the share of the first three.

Oil and gas processing

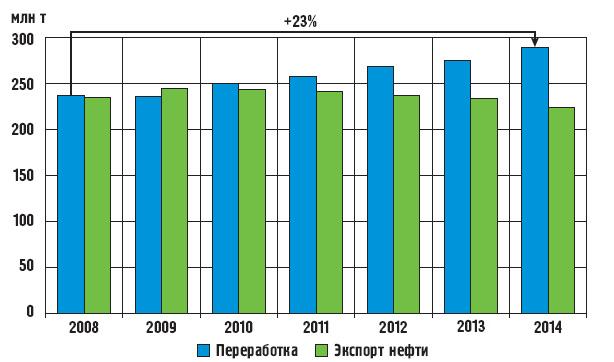

The production of petroleum products and gas processing products is one of the most important components of the oil and gas industry. At the end of 2014, 288.7 million tons of oil and more than 70 billion cubic meters were sent for refining in the Russian Federation. meters of natural gas. At the same time, the amount of oil sent for oil refining increases every year in comparison with oil sent for export. In 2012, the difference between refining and oil exports was 26 million tons, in 2013 this figure increased to 37 million tons, and in 2014 it reached 67 million tons.

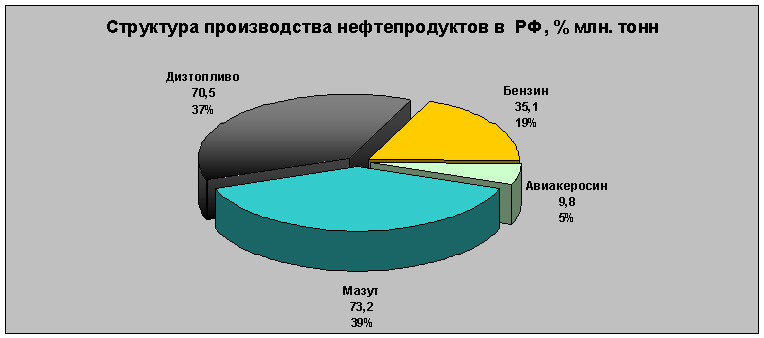

At the end of 2014, the refineries of the Russian Federation produced:

- Motor gasoline - 35.1 million tons;

- Diesel fuel - 70.5 million tons;

- Fuel oil - 73.2 million tons;

- Aviation kerosene - 9.8 million tons.

About 60% of the produced petroleum products in 2014 were exported. In quantitative terms, the volume of exported oil products amounted to 165.3 million tons for a total of 115.8 billion US dollars. The total export value of petroleum products is 72% of the amount received for the export of crude oil. For comparison, this indicator in 2000 was 44%, in 2005 - 40.7%, in 2010 - 51%, in 2013 - 62.5%. It should also be noted that more than 94% of oil products in 2014 were exported to non-CIS countries. Thus, we can state the fact that every year Russian oil products are becoming more and more interesting for foreign consumers, and every year the position of Russia as the main world exporter of oil products is strengthening.

The amount of liquefied gas exported by the Russian Federation in 2014 is 20.5 million cubic meters. meters. This is 22% less than the same indicator in 2013, when a record amount of liquefied gas was exported - 26.3 million cubic meters. m. Compared to the export of natural gas, the total cost of export of liquefied gas is 11 times less. In 2014, liquefied gas was exported in the amount of $ 5.2 billion.

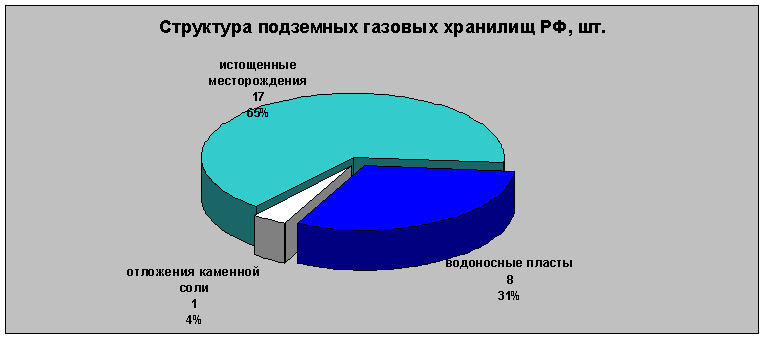

In addition to the transportation and processing of natural gas, it is necessary to ensure the storage of this type of fuel. For its storage, special underground storage facilities are used. There are 26 underground gas storage facilities in the Russian Federation, of which the largest is Kasimovskoye, which is located in the Ryazan Region. It can hold 11 billion cubic meters. meters of natural gas. Storage facilities are located, as a rule, in the main areas of gas consumption. In the Russian Federation, underground storage facilities are being created in depleted deposits (the most popular technology), in aquifers and in rock salt deposits.

Underground gas storage facilities are located mainly in the European part of Russia. There are especially many storage facilities near Samara - 4 units (Dmitrievskoye, Amanakskoye, Mikhailovskoye, Kiryushinskoye), Saratov - 3 units (Peschano-Umetskoye, Elshano-Kurdyumskoye, Stepnovskoye), Orenburg - 3 units (Kanchurinskoye, Musinskoye, Sovkhoznoye).

Today there are 26 gas processing plants in the Russian Federation. According to this indicator, Russia significantly lags behind the United States, where more than 520 such enterprises operate. But it should be noted that in Russia gas processing is carried out at large plants, while in the USA the lion's share Gas processing plants are made up of installations located directly in the fields, the main function of which is to prepare for the transportation of gas to large plants.

The largest gas processing plant in Russia and in the world is the Orenburg Gas Processing Plant. Its production capacity allows it to process 15 billion cubic meters. m per year. Other large factories in the country are Astrakhan and Sosnogorsk. These three plants account for more than 95% of the processing of all associated gas that is formed in oil reservoirs.

There are about 100 enterprises in the oil refining industry of the Russian Federation. 38% of them are oil refineries belonging to vertically integrated companies, they produce about 85% of all petroleum products. 14% of the total are independent refineries, which produce 11% of the products. Mini-refineries account for 48% of the total number of enterprises, and they produce 4% of Russian oil products.

Most of the oil refineries are part of the structure of the Rosneft company - 9 units, the total production capacity of which is 77.5 million tons. And the largest Russian refinery is Kirishsky, with a production capacity of 22 million tons, owned by Surgutneftegaz. Other large factories in the country are the Omsk Refinery (production capacity 21.3 million tons / year), Lukoil-Nizhegorodnefteorgsintez (production capacity 19 million tons / year), Yaroslavnefteorgsintez (production capacity 14 million tons / year).

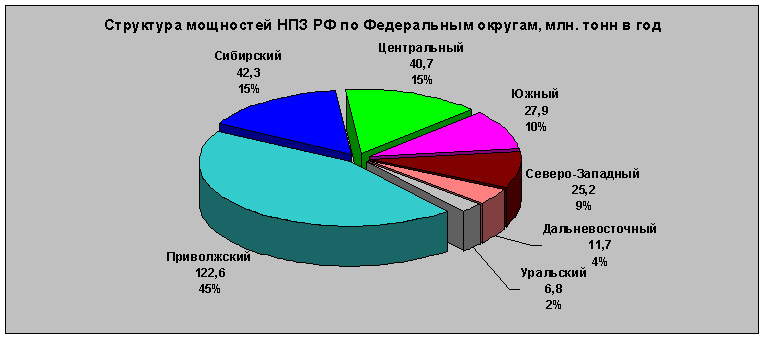

Most of the country's oil refineries are located in the European part of Russia. This is because it is much cheaper to transport crude oil than petroleum products. As a rule, refineries are located in cities where there are river ports in order to save on transport costs, since delivery by water transport the cheapest. Distribution of capacities of oil refineries by Federal districts Russian Federation looks like this:

- Central Federal district- 40.7 million tons;

- Northwestern Federal District - 25.2 million tons;

- Ural Federal District - 6.75 million tons;

- Volga Federal District - 122.6 million tons;

- Far Eastern Federal District - 11.7 million tons;

- Siberian Federal District - 42.3 million tons;

- Southern Federal District - 27.9 million tons.

The largest oil and gas companies in Russia

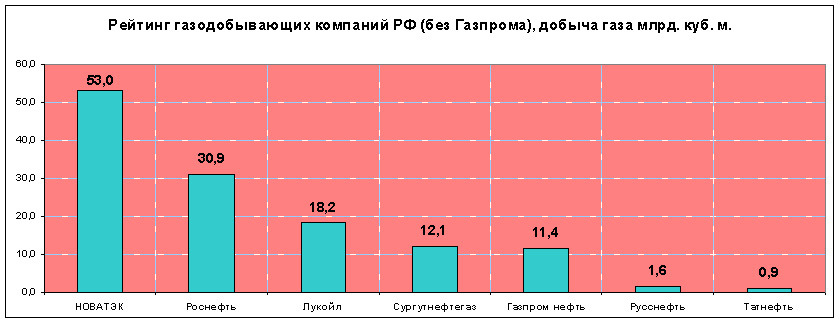

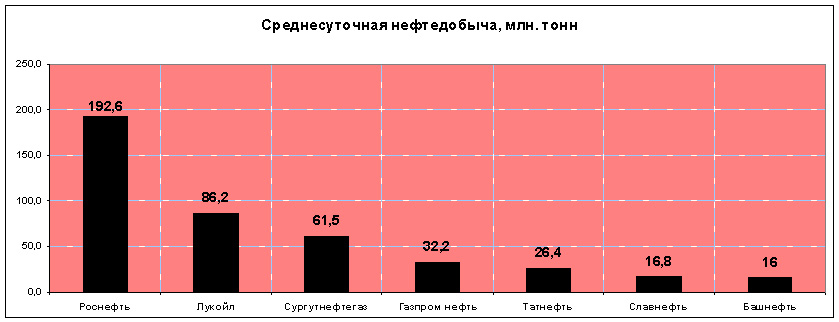

OJSC Gazprom and the company NOVATEK are the largest Russian companies engaged in the production and processing of natural gas. In addition to them, natural gas production is also carried out by enterprises that are part of the structure of vertically integrated oil companies. As for the oil industry, the leader here is Rosneft, and apart from it, the leading positions in the market are occupied by Lukoil, Surgutneftegaz and Gazprom Neft.

OJSC Gazprom is the flagship Russian economy, a company whose annual turnover exceeds the budget of some European countries. Gazprom controls over 150,000 km of gas pipelines and 22 underground gas storage facilities. OAO Gazprom is developing all the largest fields in the Russian Federation (except for Yurkharovskoye). It is the only Russian company that has the right to export natural gas.

Gazprom's turnover in 2014 amounted to 5.661 trillion. rubles, while the company amounted to 1.31 trillion. rubles. The number of employees of OAO Gazprom is about 430 thousand people.

NOVATEK is the second largest natural gas producer in Russia. The headquarters of the company is located in the city of Tarko-Sale (Yamalo-Nenets Autonomous District). NOVATEK is developing at Yurkharovskoye, Vostochno-Tarkosalinskoye, Khancheyskoye and other fields located in the Yamalo-Nenets Autonomous District.

In terms of total revenue, NOVATEK is significantly inferior to Gazprom. At the end of 2014, the company's turnover amounted to 357.6 billion rubles. amounted to 125.1 billion rubles. NOVATEK controls 7.9% of the Russian gas market and employs about 4,000 people.

The largest Russian oil company is Rosneft. The company produces oil from the largest oil fields in Russia - Priobskoye, Samotlorskoye and Vankorskoye. The oil refining industry of the company includes 9 large oil refineries and 3 mini-refineries.

At the end of 2014, Rosneft's turnover amounted to 5.1 trillion. rubles, the total profit is 593 billion rubles. The number of the company's employees exceeds 170 thousand people.

Lukoil is the second largest Russian oil company in terms of production. For more than 10 years, Lukoil held a leading position in the market, but in 2007 lost the leadership to Rosneft, after its takeover of Yukos. Lukoil produces oil in the Khanty-Mansi Autonomous Okrug, the number of operating drilling rigs of the company is more than 27,000. The oil refining industry is represented by 4 large refineries with a refining capacity of 45.6 million tons.

The total turnover of the company at the end of 2014 amounted to USD 144 billion, operating profit is USD 7.2 billion. The company employs over 150,000 people.

Surgutneftegaz is the largest oil company in the Russian Federation, headquartered outside of Moscow. The structure of the company includes the largest Russian refinery - Kirishsky. Largest deposits developed by "Surgutgutneftegaz" - Lyantorskoye and Fedorovskoye.

At the end of 2014, the turnover of Surgutneftegaz amounted to 862.6 billion rubles, equal to 241 billion rubles. The company employs about 110 thousand employees.

Gazprom Neft is an oil company, 95.68% of which is owned by Gazprom. Gazprom Neft, together with Rosneft, is developing the Priobskoye oil field. Over the past year, the company's oil refining industry produced 43 million tons of oil products.

The company's turnover for 2014 is 1.7 trillion. rubles. amounted to about 122 billion rubles. The company employs over 57 thousand people.

Industry development prospects

The rate of development of the oil and gas industry in the Russian Federation largely depends on world oil prices and on the behavior of the main competitors in oil production on the world market - Saudi Arabia and the USA. These three countries are constantly replacing each other as leaders in oil production. At the beginning of 2014, Saudi Arabia was the leader with 11.72 million barrels of oil per day. At the end of 2014, the first place went to the United States - 11.6 million barrels per day, Saudi Arabia ended the year with an average of 11.5 million barrels per day, Russia was third - 10.8 million barrels per day. At the end of 5 months of 2015, the Russian Federation kept production volumes at about the same level and became the leader. As of the end of May this year, the Russian Federation produces an average of 10.75 million barrels per day, Saudi Arabia - 10.25 million barrels, and the United States - 9.6 million barrels.

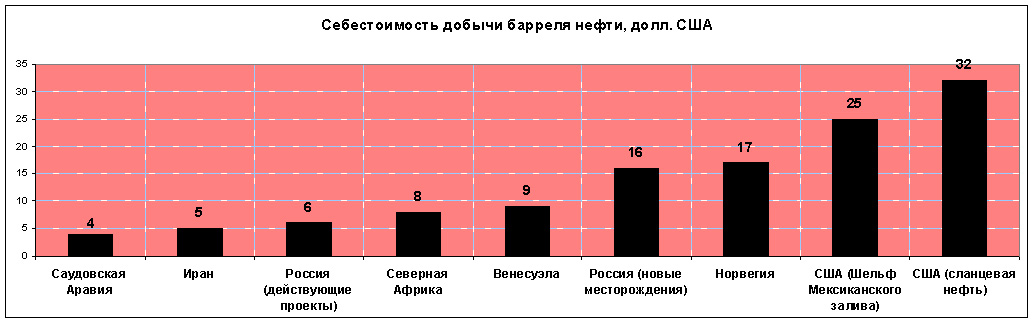

But the amount of oil produced in a given country is not a determining indicator. It is influenced by the percentage of oil produced in the leading oil powers. This is due to the fact that the production of 1 barrel of oil in different regions significantly different. The lowest in Saudi Arabia and Iran, and the most expensive in the United States.

Thus, with a decrease in the level of production of cheap oil in the Middle East, in order to meet world needs, expensive oil begins to be produced in large volumes from offshore fields, which leads to an increase in the cost of a barrel in exchange trading.

It is easy to guess that an increase in large volume of oil production by Saudi Arabia and other OPEC members with low production costs will bring down world oil prices. And if the cost of a barrel of oil reaches $ 30-35 and fixes itself at this level for a long time, then the US oil industry will face a financial collapse.

Of course, the use of tough dumping by OPEC countries on the world oil market is unlikely, since this could lead to a deep financial crisis, which will largely affect the oil exporters themselves, whose government revenue depends on the price of “black gold”. As for the Russian Federation, the price of $ 25-30 per barrel is not critical for the oil and gas industry, since the cost of export oil, together with transportation, averages $ 23 per barrel. But although the price of $ 30 per barrel will allow the leading oil companies of the Russian Federation to stay "afloat", the federal budget will be missing several trillion rubles, which could have catastrophic consequences for the country.

In order to protect themselves as much as possible from fluctuations in oil prices, Russian oil and gas companies are increasingly paying attention to the development of energy exports to the countries of Southeast Asia, Japan, China and India. The countries of this region have great economic potential and for its realization are forced to export oil and gas in huge quantities. In addition, a very important factor is the fact that most of the oil and gas fields are located in Siberia, from where transportation of fuel to the Pacific region is cheaper than to Europe. The only problem, on which work has already begun, is the weak capacity of the oil and gas transportation system in the eastern direction. To solve transportation problems, the Eastern Oil Pipeline has already been put into operation and the Power of Siberia gas pipeline is under construction.

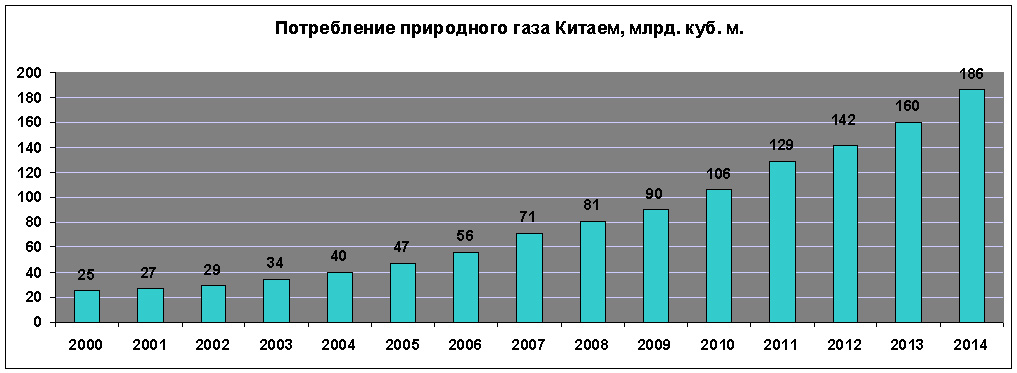

According to experts, consumption of natural gas in China in 2030 may reach 600 billion cubic meters. meters, which will exceed the gas consumption of all European countries taken together. Now China's consumption is 186 billion cubic meters. m., and European countries - about 540 billion cubic meters. meters. The dependence of Europeans on Russian natural gas and oil is very high, because even the package of sanctions against the Russian economy did not affect energy exports.

If South-East Asia, China and India will go at the same pace as now, then the European sales of gas and oil for Russia will become secondary, and the bulk of energy will be directed to the east. In this case, European countries risk becoming more dependent on Russian gas than they are now. After all, on this moment depends on gas and oil exports to Europe as much as European economy from the import of these minerals. And in the event of a reorientation of the oil and gas industry of Russia to the "eastern vector", the dependence of the Russian Federation will decrease, and the need of Europe will not go anywhere. And as the head of Gazprom, Alexei Miller, noted at the International Business Congress held in May 2015 in Belgrade, “there are no competitors for Gazprom when supplying gas over a distance of 10,000 km. to the European market ”.

This year, the energy theme is firmly entrenched in the leading articles of economic publications. The events in Ukraine and Iraq make us think again about who controls gas and oil today. Our list includes the ten largest oil and gas companies in the world, on which the well-being of the global economy directly depends:

11. Fuel Corporation of Kuwait: 3.2 million barrels per day

The company was formed in 1934 by UK and US players who today operate under the names BP and Chevron. In 1975, the Kuwaiti authorities seized the initiative from foreigners and established control over oil production, and by 1980 completely nationalized the energy industry. During the Gulf War, the company's assets were severely damaged and production recovered slowly. However, today Kuwait is one of the most stable states in the Middle East and produces enough oil and gas to occupy 10th place in our ranking.

10. Chevron: 3.5 million barrels per day

An American company that has changed both its name and set of assets more than once over its long history. After oil was discovered in California in 1879, a player called the Pacific Coast Oil Company emerged to take over Star Oil's assets. After a huge number of acquisitions and reorganizations, more than a century later, in 1984, the two companies of which PCOC was an ancestor, Standard Oil of California and Gulf Oil, merged. This merger was the largest in history at the time. The common cause of the two companies was named Chevron. And in 2001, the player became even stronger following the purchase of Texaco. In 2010, Atlas Petroleum was acquired for $ 4.3 billion. With so many assets, Chevron has survived to this day. The company operates in 180 countries. In addition to gas and oil, she is engaged in geothermal energy sources.

9. Petroleos Mexicanos (Pemex): 3.6 million bpd

The basis for the formation of the oil industry in Mexico was the activities of the British and American companies, which at the beginning of the 20th century began to actively develop deposits on the territory of the country. In 1938, the state supported the striking workers and nationalized the entire energy sector. Today, a third of Mexico's budget revenue comes from giant Pemex, which, like many other fuel companies, is the country's top taxpayer. V last years Pemex collided with a number emergency situations and some of the company's managers have been accused of corruption.

8. Royal Dutch Shell: 3.9 million barrels per day

The British-Dutch oil and gas giant, created in 1907 as a result of the merger, The company remains one of the most versatile in the gas business, as it develops fields around the world and produces a huge number of products, including the popular LNG today. Shell also invests in solar energy and wind turbines. The company's revenue in 2013 reached an impressive $ 450 billion.

7. BP: 4.1 million barrels per day

The history of British Petroleum, which today prefers to call itself simply BP, dates back to 1909, when the Anglo-Persian Oil Company was formed. For a hundred years, the British managed to develop a huge number of deposits all over the world, including in the Gulf of Mexico. Alas, here BP suffered a setback, and after an accident on an oil platform in 2010, the company had to sell assets to cover losses. Recall that the company gave up its stake in TNK-BP and sold it to Rosneft in March 2013. After the accident in the Gulf of Mexico, BP, which occupied the second place in the world ranking, rolled back, but still demonstrates impressive production volumes.

6. Rosneft: 4.1 million barrels per day

Rosneft is the world's largest public company in terms of oil production. It was created on the basis of a state player called Rosneftegaz, which emerged from the wreckage of the Soviet oil and gas industry. The company's revenue under IFRS for 2013 amounted to RUB 4.694 trillion, which reflects an increase of 52% compared to the previous year. The production of oil and liquid hydrocarbons averaged 4.176 million barrels per day in 2013, which reflects an increase of more than 70% compared to 2012. Such a sharp rise is due to the purchase of TNK-BP. Rosneft cooperates with major foreign companies. The alliance with BP did not materialize after the disaster in the Gulf of Mexico, but an agreement was concluded with ExxonMobil. Rosneft is the largest taxpayer in Russia.

5. Petrochina: 4.4 million barrels per day

Petrochina was founded in 1999, but it occupies a high position in our rating, as it received the lion's share of the oil and gas assets of the Celestial Empire under management. China is trying to concentrate in its hands assets from around the world, trying to keep up with the ever-growing demand for fuel from its industry. In such a situation, Petrochina becomes a tool for concluding transactions not only for the sale of gas, but also for the purchase of raw materials, as well as shares in fields. Recently, experts have been saying that Petrochina may start developing shale deposits in the PRC.

4. ExxonMobil: 5.3 million barrels per day

When John Rockefeller was forced to split his oil empire, Standard Oil Company, two new players entered the market - Standard and Socony. They later morphed into Exxon and Mobil, and eventually merged into ExxonMobil. The merger was completed in 1999. Today it is the largest US player, with oil and gas sales of over $ 400 million per year. Net profit reaches $ 30 billion. There were also problems, such as the crash of the tanker Exxon Valdez in 1989, but the company continues its international expansion.

![]()

3. National Oil Company of Iran: 6.4 million barrels per day

The Iranians could also thank Great Britain for creating their oil and gas industry, which at the beginning of the 20th century got here as part of the activities of the Anglo-Persian Oil Company. But Iran hardly considers foreign actions to be a service. After the revolution of the late 70s. the country nationalized their assets, accusing them of trying to steal Iran's national wealth. The National Oil Company was founded back in 1951, when nationalists came to power in the country and tried to drive out the British for the first time. But it was only after 1979 that Iran was able to turn its own oil company into a single powerful structure, which receives huge revenues even against the backdrop of sanctions.

2. "Gazprom": 9.7 million barrels per day

Gazprom is the world's largest company specializing in the production and transportation of gas. The shares are held by both private investors and the state, which has concentrated in its hands the lion's share of the securities. The company's revenue reaches $ 150 billion, and its profit is $ 40 billion. Gazprom helps Russia to maintain the title of one of the largest exporters energy resources. The last major agreement was a contract with China for the supply of gas for 30 years, totaling $ 400 billion.

1. Saudi Aramco: more than 12 million barrels per day

Saudi Aramco is the national oil company of Saudi Arabia. The largest oil company in the world in terms of oil production and the size of oil reserves. Its history began in the 30s. last century, when Standard Oil of California drilled the first oil wells in Saudi Arabia. The name Aramco itself stands for "American Arab Oil Company". However, after the cooling of relations between the United States and Saudi Arabia because of Israel, the Saudis decided to take their fuel industry under control and by 1980 squeezed the Americans out of it, adding the prefix Saudi to Aramco. The company is rightfully ranked first in our rating by a wide margin from its pursuers.

Impossible to imagine modern world without refined products. Various types of fuel, medicines, road surfaces and even children's toys are direct or indirect products of the oil industry.

Oil companies are strategically important sources of budget replenishment for most states that have a sufficient number of fields. As statistics show, the largest oil producing companies in Russia, even with a significant drop in hydrocarbon prices in the world, continue to work with profit.

World oil production

Analysts, based on statistical data on the volume of oil production in the world, distinguish two stages in the development of the industry:

- The first - from the very beginning to the first relative maximum, which was reached in 1979 (the volume of oil produced was 3235 million tons).

- The second stage lasts from 1979 to the present time.

From 1920 to 1970, there was a steady increase in world oil production with annual growth. If we combine the data for decades, then the growth in production occurred in geometric progression, that is, it doubled every 10 years. Since 1979, after peaks, oil companies have slowed down production growth. In the first half of the 1980s, there was even a short-term decline in oil production. In the future, the increase in the volume of oil produced is resumed, although not as rapidly as at the first stage.

Oil production in Russia

Oil and gas production in Russia is a strategic foundation of the economy, an outpost of stability and a base for the development of many industries. Due to its significant share (over 12%) in world oil production, Russia occupies one of the leading positions in the global energy security system. Oil companies are connected by a complex set of interactions that provide the path of crude oil from the field to the gas tank of a car or any enterprise that uses refined products as raw materials.

The oil giants of Russia are solving dozens of economically important tasks for the country. The functioning of the oil complex, which includes the production and processing of hydrocarbons, is ensured by a developed system of subsidiaries of leading companies. But despite the relative versatility of the leading oil conglomerates, they have certain specific features associated with economic and even natural conditions... In this regard, leading Russian companies often engage third-party small oil companies for the construction and maintenance of wells, auxiliary facilities, pipelines, and other tasks. The influence of some companies extends throughout the territory of the Russian Federation and partially to foreign countries... Many companies have a strictly regionalized resource base.

The largest vertically integrated oil companies in Russia

About 90% of all oil produced in Russia is accounted for by 9 large oil companies with a vertically integrated structure: Rosneft, Lukoil, Gazpromneft, TNK-BP, Tatneft, Surgutneftegaz, Bashneft, Slavneft "," Russneft ". In addition, there are about 150 small and medium-sized mining enterprises. The largest oil companies are vertically integrated. In the oil business, this means combining all the necessary links for the functioning of the technological chain of the movement of hydrocarbons from production to processing:

- geological exploration of reserves, drilling of wells, arrangement of fields;

- extraction and transportation of crude oil;

- processing and transportation of finished petroleum products;

- sale of petroleum products.

In terms of oil production, the industry leaders in Russia are Rosneft and Lukoil.

Rosneft

Rosneft was established on the basis of the State Ministry of Industry in the early nineties. The transformation into a joint-stock company made it possible to raise additional funds and introduce a large number of small oil-producing companies in Russia into the company. Over time, small businesses became large subsidiaries within a huge holding. The controlling stake (50.1%) belongs to the Russian Federation, 9.75% - to the British company BP; 19.5 - to an international consortium (Switzerland, Qatar); 7.5% - rotate in the form of depositary receipts. As of December 2016, the company's capitalization amounted to $ 57.6 billion (according to the MICEX). The volume of oil produced exceeds 5,000 million barrels per year.

Lukoil

One of the largest oil and gas companies in Russia. The main activities are hydrocarbon production, oil refining, petrochemical production, sales of end products. Lukoil is one of the first joint stock companies in Russia. The holding includes 45 subsidiaries in almost 20 countries of the world. 25 large oil fields are being actively developed, most of which are located in Western Siberia. In 2012, having bypassed such competitors as Rosneft and Gazprom, the company obtained the right to develop fields in the Khanty-Mansi Autonomous Okrug.

Lukoil is one of the leaders in oil refining; the company includes 4 oil refineries. Most of the products are sold on foreign markets in neighboring countries, Eastern and Western Europe, USA. In 2009, Lukoil paid a fine of 6.5 billion rubles, as ordered by the Federal Antimonopoly Service, for actions that led to an increase in prices for oil products. The annual production of liquid hydrocarbons is almost 900 million barrels. Capitalization for December 2015 - $ 35.5 billion.

Fast-growing companies

According to the RBC rating, the Irkutsk Oil Company (INK) occupies a leading position among the fastest growing companies in Russia. Over the past few years, INK has increased the volume of oil produced by almost 5 times, to 2.9 million tons, and revenue - 9 times. The independent company was established in 2000, bringing together three large oil producing structures:

- Danilovo Oil Company LLC - specializes in geological works and oil production at the Danilovskoye field.

- OJSC UstKutNeftegaz is a company that owns areas with huge reserves of hydrocarbons at the Markovskoye and Yaraktinskoye fields.

- LLC INK-NeftegazGeologiya is a leading developer of hydrocarbon fields in the Irkutsk region. Specializes in exploration and geological research of deposits, oil production.

From the very beginning of their work, INK has relied on new technologies and highly qualified personnel. Also, in many respects, the company's success is associated with the close proximity to the raw materials assets of the ESPO pipeline (Eastern Siberia - Pacific Ocean). Obtaining a permit for connection to the pipeline made it possible to significantly increase the volume of oil produced.

SMALL AND MEDIUM INDEPENDENT OIL COMPANIES

AS A CARRIER OF COMPETITIVE ADVANTAGES

postgraduate student of the Department of Economic Theory

Financial Academy under the Government of the Russian Federation

Position of NOCs in Russia

Small oil business in our country originated in the 1990s. Initially, the sector experienced rapid growth, but now the number of small and medium-sized enterprises is constantly decreasing. Currently, the total number of independent oil companies in Russia is about 160, but only 50 can be called truly independent. Nevertheless, Russian NOCs produce more than 4% of all oil in the country, and according to experts, this figure will grow.

According to the Association of Small and Medium Oil and Gas Producing Organizations "AssoNeft", the share of NNK products in 1995-2006. in the total volume of the country ranged from 4% to 10%, and during this period they produced about 300 million tons of oil, and in 2006 alone, small companies produced about 19.9 million tons of oil. However, even such significant indicators do not fully reflect the real contribution of NOCs to industry-wide production, since during the period under review they were absorbed by large vertically integrated oil companies. If there were no mergers and acquisitions (i.e., while maintaining the numerical strength of the NOC as it was at the beginning of 2000), the estimated oil production by independent oil companies in 2006 would have amounted to more than 60 million tons.

If we compare the dynamics of development of NOCs and VOCs, then it should be admitted that, despite the small size of the business, the small oil sector demonstrates outstanding results. For example, the growth in oil production in 2005 compared to 2004 for vertically integrated companies was 1.5%, for the industry as a whole - 2.5%, and for small companies - 18.9%. Due to the increase in the domestic oil price, which made the NOC business more profitable, in 2006 this growth gap not only did not narrow, but widened. Thus, production in the NOC sector increased by 19.4%, in the industry - by 2.2%, in the vertically integrated oil companies - only by 1.1%. It can be said that tiny and low-power NOCs gave the same increase in production in absolute terms as all vertically integrated oil companies combined.

Regionally, in 2006, 3/4 of all oil (74.2%) NOCs produced in the Khanty-Mansi Autonomous Okrug, Tatarstan and Komi. As of January 1, 2007, it was here (plus the Orenburg region) that 91 independent oil enterprises were located, that is, 59.5% of their total number. Another five regions (Tomsk, Kalmykia, Samara, Saratov, Udmurtia) operated 31 companies. In total, these nine regions account for about 4/5 of independent oil producers (122 organizations or 79.7%).

What are the specific features of NOCs' activities?

First, as already mentioned, the nature of the fields being developed is noteworthy. The resource base of the NOC includes insignificant deposits, low-profitable subsoil areas, residual reserves. These are small and medium-sized deposits with difficult mining and geological conditions, with a high proportion of hard-to-recover reserves. Note that large companies prefer to leave depleted oil fields for richer ones, since it is simply inappropriate to exploit small and hard-to-recover reserves within the framework of oil holdings.

How serious this problem is can be judged by the presence of several thousand "ownerless" wells in the country. The essence of this phenomenon is as follows: an unexploited well after several years becomes a source of environmental pollution and inevitable fines. Therefore, vertically integrated oil companies prefer to deny ownership of such wells under any pretexts. Accordingly, NOCs, in addition to their own production functions, also perform the role of a kind of "cleaners" for VIOCs: in many cases, they develop fields inherited from the oil giants.

It should also be borne in mind that due to the specifics of geological conditions in our country, it is precisely small deposits that quantitatively prevail (small deposits account for about 80% of all explored ones). Such deposits are not of interest for large oil holdings, but they are important for the owner of the subsoil, the state, based on the principle of maximum extraction of oil from the subsoil. NOCs operate in such fields, transferring them from the category of unprofitable to profitable, using an individual approach to each field, applying modern methods of development and production.

In the apt expression of A. Kuptsova, small oil companies are a kind of "orderlies of the subsoil". They are working on depleted deposits that are at a late stage of production. Unlike large companies, they do not skim the "cream" from the wells and do not throw it when they come to the "difficult oil", but produce it carefully and accurately.

Secondly, small companies are mono-commodity producers. Their only commodity is crude oil, and their main income comes from selling it. NOCs, as noted, usually do not have their own refining facilities. In the conditions of Russia, where, as you know, oil refineries that are not part of the VIOC are experiencing constant oil hunger, this circumstance turns the NOC into important factor stabilization of domestic oil refining and petrochemistry.

Thirdly, NOCs act as a kind of “efficiency indicator” of the mining business. Small companies are much more transparent, since they have a much simpler structure (there are no numerous levels of vertical integration, there is no loop of dependent and semi-dependent subcontractors, etc.). In addition, NOCs do not have lobbying resources and the ability to create schemes to “optimize” taxation. Finally, it is impossible to imagine that they dictate prices for gasoline and oil products, as sometimes vertically integrated oil companies do.

For small companies, the state can establish what the real cost of oil production is, and, accordingly, how much tax revenue should be from each tonne produced. NOCs are characterized by the highest specific tax deductions. For years. they contributed more than $ 18 billion to the federal budget, and about $ 7.2 billion to local and regional budgets.

Competitive advantages and weaknesses of NOCs

Small oil companies have certain competitive advantages that allow them to successfully carry out their activities and develop.

1. NOCs are flexible and mobile - because it is easier for a small company to adjust its plans and make changes in its activities in a constantly changing business environment.

2. As we have already mentioned, the only commodity of NOCs is crude oil. In turn, the mono-commodity nature of production helps to reduce costs.

3. An individual approach to the development of each field allows to achieve higher efficiency of activities.

How can you explain the company's success? It consists of several components.

First, local knowledge. The company operates in one single region, and is well aware of its features. Specificity geological structure Eastern Siberia consists in the fact that its subsoil layers are fragmented into small parts, which leads to the fragmentation of deposits. In addition, the region as a whole is characterized by an extremely low level of exploration. Therefore, the development of the subsoil of Eastern Siberia may be of interest to just such small companies as INK, which are capable of exploration and development of small reserves.

Secondly, efficiency in decision-making. “In most large corporations, due to bureaucratic obstacles, decision-making can take months, while the INC has always focused on operational decisions,” says Marina Sedykh. prompt response to the situation ".

Thirdly, the possibility of occupying a niche, the scale of which is not suitable for large companies, or does not fit into their concept. “Most large companies will not consider projects that bring in 'just', say, hundreds of thousands of dollars,” she says. “In our country, along with the fact that key projects remain in the focus of managers, medium-sized projects are also considered not only as possible sources of profit, but also as additional larger-scale plans.” INK has managed to occupy its own niche in oil production and will be able to take advantage of the previously indicated advantages that are inherent in small oil companies.

The key success factor, in our opinion, is a competent company strategy. The main problem for small oil companies, as we have already mentioned, is the lack of infrastructure, primarily transport, both roads and pipelines. Indeed, in order to develop a field, it is necessary to be able to reach it and bring equipment, and the extracted oil must be somehow removed. This is what stops many companies because investing heavily in infrastructure from scratch is risky. After all, if, for example, when assessing the reserves of a field, an error was made and the real reserves are less than expected, then the company will incur losses. The money has already been invested in the construction of the pipeline, but there is nothing to extract!

On the other hand, usually the company buys the right to develop a certain area, which may contain several small deposits. In this case, the construction of the pipeline will link them together. In addition, during additional exploration, additional, previously unnoticed oil reserves may be discovered. At the same time, the total volume of production can be significant.

So, having made the decision to create its own infrastructure - first of all, the construction of pipelines - the company solved the problem of transporting the produced oil, which served as a strong incentive to increase production.

Prospects for the development of NOCs in the Russian Federation

So, we examined the position of NOCs in our country, the specifics of their activities, the competitive advantages and weaknesses of NOCs. Our research has shown the importance of NOCs for increasing the competitiveness of the Russian economy, and the successful development of the Irkutsk Oil Company is proof of this.

What are the prospects for the functioning of the NOC?

Since producing “difficult” oil from wells is a natural niche for small oil companies, “small companies have growth potential. Each small company has its own niche, which provides it, subject to certain conditions, an autonomous life, within which it is possible to develop very well. The experience of our company shows that such regional companies are needed to develop small oil and gas fields. We live here, pay taxes here, it is easier for us to interact with the authorities, it is easier to build a business. Large holdings are focused on obtaining greater profits, so small areas are not of interest to them. If we talk about takeovers, then we receive offers to buy, but we are in no hurry to sell the company, because we didn’t come to get money, but to work, to do something significant, important, to build a successful business right here in our region ”. This is the opinion of M. Sedykh, and we subscribe to her opinion.

N. Ilyin, who held in 2003. the post of Chairman of the Committee for Subsoil Use and Oil and Gas Complex of the Department natural resources and the oil and gas complex of the Administration of the Tomsk Region, he is also confident in the prospects of small oil companies: “ Large companies it is unprofitable to engage in small deposits, since this entails a decrease economic indicators, and they are not interested in this. Consequently, the niche of small business in the oil industry will be present. Acquisitions can only affect those who have high prospects for production volumes: large reserves, proximity to main oil pipelines, and there are no such, at least in the Tomsk region, ”.

Once again, we note that the creation, development and effective functioning of NOCs is extremely important for increasing the competitiveness of the economy of our country. It is easy to see, however, that the benefits from their operation are concentrated mainly at the national level (more complete use of resources, "cleaning up the tailings" for vertically integrated oil companies, social sustainability, etc.). At the same time, difficulties (poor deposits, isolation from the most profitable ways of selling products, etc.) have to be borne exclusively by the NOCs themselves. Obviously, under these conditions, state support for NOCs and the creation of more favorable conditions for their activities, especially at the initial stage of the emergence of small and medium-sized businesses in the oil and gas sector, becomes relevant. . Russia should take into account the international experience of NOCs functioning. So, if a hundred years ago, the seven largest world oil producing enterprises controlled 90% of recoverable hydrocarbon reserves, but now their share is less than 10%. In general, there is a tendency in the world to form small specialized oil companies and decentralize their activities.

Many representatives of small oil companies see the possibility of state support in only one thing - preferential access to export pipelines. Since the main income of NOCs derives precisely from the export of crude oil (selling oil to the domestic market - to refineries - is extremely unprofitable), the only way to increase profits for small companies is to increase the export of their products. Recall that vertically integrated oil companies are in a more advantageous situation here, since they export not only crude oil, but also petroleum products.

Without disputing the described method of supporting NOCs, we note that, despite its popularity among small firms themselves, it should by no means be considered as the only possible one. For example, a positive result could be provided by providing access for small and medium-sized businesses to profitable internal channels for the sale of oil. Vertically integrated oil companies create complete production cycles - from exploration to refueling at their own gas stations. It is imperative for small businesses to have access to the links in this production chain.

So, the state should provide large political and economic support to small and medium oil companies. It seems justified to use a set of protectionist measures to ensure the growth of NOCs at the initial stage. Thus, the functioning of NOCs will contribute to the development of the regions, which will have a beneficial effect on the growth of the economy of the entire country.

Literature

1. Korzun E. Big opportunities of small companies // World energy. - 2007. - №8.

2. Korzun E. Independent oil companies of Russia: myths and reality // Economy and fuel and energy complex today. - 2007. -№2.

3. Kuptsova A. Subsoil orderlies // Continent Siberia. - 2007. -№48.

4. Maslova O. “Little kids” and “giants”: who is the future for? // News of Ugra.-2002.- №83.

5. Prokopenko D. Oil "kids" need support // Nezavisimaya Gazeta.-2001.-№ 000.

Timakova N. The great importance of small companies. Interview with the head of the "Nobel Oil" Oil Company G. Gurevich // World Energy. - 2005. - No. 7-8.

7. Website of the Irkutsk Oil Company - www. *****

Russian newspaper

http: // www. ***** / archive / 2005/06/22/203790 This year oil will go through the BAM - Marina Sedykh

Interview with the general director of the oil company "

The largest oil and gas companies in the world in terms of hydrocarbon production. The ranking is interesting precisely because it provides data on both oil and gas production converted to conventional barrels of oil per day. This approach makes it possible to compare companies with different production structures within the same list and understand which of them is “larger”.

The second feature of the ranking is the inclusion of not only public and partially state corporations, but also completely state corporations, which journalists often forget. But it is the state-owned companies and even the oil and gas ministries of individual countries that often produce more oil and gas than well-known private giants.

In developing its hydrocarbon production, Russia is following a hybrid path: the formation of huge state-controlled companies with multibillion-dollar revenues and an opaque system of expenses, combined with the presence of a small number of private investors. At the same time, the fact that some of the shares of mega companies are traded on stock exchanges makes it easier for them to obtain loans and evaluate their shares in exchange transactions of the Rosneft-BP type. offers a translation of the ranking published on forbes.com, with its explanations and additions.

1. Saudi aramco- 12.5 mln b / d (conventional barrels of oil per day)

State Oil and Gas Company of Saudi Arabia. In fact, it acts as a balancing force in the world oil market, increasing and decreasing production depending on the movement of exchange prices.

2. Gazprom- 9.7 million bpd

Russian company controlled by the state. The bulk of the hydrocarbons produced is gas, although Gazprom owns almost 100% of the shares of the large oil company Gazprom Neft (formerly Sibneft). The state, through several legal entities, owns slightly more than 50% of Gazprom's shares. However, the real power in the company belongs to a group of managers closely associated with the "St. Petersburg" political and business group. Gazprom's financial flows are serviced by a private Gazprombank controlled by the Rossiya bank from St. Petersburg, the so-called “Vladimir Putin’s friends bank”; construction contracts are carried out by companies of the same group, the country's largest insurance group SOGAZ, which is part of Gazprom’s “perimeter”, belongs to the bank "Russia"...

3. National Iranian Oil Co.- 6.4 million bpd

Fully state-owned Iranian corporation. Recently, it has experienced sales difficulties due to sanctions imposed on oil exports from Iran by Western countries. Nevertheless, Iran successfully cooperates with India, Turkey and China, supplying them with oil in exchange not only for dollars, but also, for example, for gold or yuan.

4. ExxonMobil- 5.3 million bpd

The largest private oil and gas company in the world with annual revenues of about $ 500 billion. Unlike most other oil and gas corporations, it is truly global, operating in dozens of countries around the world. One of the most hated corporations in the world, mainly for tough international politics and disregard for fashion values - from "green" to "blue".

(no number) New Rosneft- 4.6 million bpd

After the merger with TNK-BP, Rosneft will become the world's largest publicly traded oil company. Gazprom and ExxonMobil, which are ahead of it in the ranking, have the main (or significant) share in the production of gas. It is sometimes mistakenly said that Rosneft will become the world's largest private oil company. This is wrong, since public status (that is, the listing of part of the shares on the stock exchange) does not mean that the company is controlled by private shareholders. Rosneft was, is and will remain under state control, despite the possible continuation of partial privatization.

5. PetroChina- 4.4 million bpd

A state-controlled Chinese oil and gas company, the largest of the three Chinese oil giants. It was once the largest publicly traded company in the world, but has fallen in price since then. In many ways it is similar to the Russian Rosneft (connections in the country's leadership, the implementation of political and economic government orders, etc.), adjusted for the scale - the Chinese company is still several times larger.

6. BP- 4.1 million b / d

British "special company" for working with unpleasant regimes. At one time, she managed to work in many "hot spots", bringing income to her country and shareholders. In recent years, he has been concentrating on oil production in the United States and Russia. Following the deal over TNK-BP, it will become Rosneft's largest private shareholder. The company's-controlled oil production will drop by almost a third as a result of this deal, but cooperation with the Russian oil near-monopoly could bring additional financial income. And there is no need to worry about BP's reputation - what's the point of worrying about something that never happened?

7. Royal Dutch Shell- 3.9 million bpd

The European equivalent of ExxonMobil is a wholly private Anglo-Dutch global corporation with traditional business ethics concepts for oil workers. Works actively in Africa and Russia.

8. Pemex(Petróleos Mexicanos) - 3.6 Mb / d

An extremely poorly managed Mexican state-owned oil producer. Despite the presence in the country of one of the world's largest oil companies, Mexico imports gasoline, since the profits from the sale of oil go not to investments in refining, but to government (including social) programs.

9. Chevron- 3.5 million b / d

An international oil, gas and energy corporation headquartered in the United States. In addition to the extraction and processing of hydrocarbons, it is engaged in the production of electricity, including actively involved in "alternative" energy projects. The main production facilities are located in the USA, Australia, Nigeria, Angola, Kazakhstan.

10. Kuwait Petroleum Corp.- 3.2 million bpd

Kuwait's state-owned oil and gas holding company, which controls many upstream and downstream companies. Oddly enough, it is very widely represented in the retail gasoline market in Denmark, Sweden, Belgium, the Netherlands under the brands Q8, OKQ8, Q8 Easy.

11. Abu Dhabi National Oil Co.- 2.9 million bpd

State Oil and Gas Company of the United Arab Emirates. Among other things, it is a major partner of the US government, including supplying fuel for US troops.

12. Sonatrach- 2.7 million bpd

Algerian state-owned company, mainly gas. Also engaged in oil production, petrochemical production and energy. One of the main competitors of Gazprom in Europe.

13. Total- 2.7 million bpd

French oil and gas company, known for its funny mustache and glasses general director Christophe de Magerie and the fact that 3% of the company's shares belong to Qatar and about the same amount to China. Total is developing the liquefied natural gas market and, quite possibly, will begin deliveries in 2015.

14. Petrobras(Petróleo Brasileiro) - 2.6 million bbl / d

More than 60% of the shares are owned by the Brazilian government, the rest of the shares are traded on the stock exchanges in New York and Sao Paulo. The Brazilian corporation made history with the largest one-time public offering of shares on the stock exchange: in September 2010, securities were sold for $ 72.8 billion. The company is fighting for the rights of whales, which does not prevent it from drilling deep-water wells in the ocean.

15. Rosneft- 2.6 million bpd

Igor Ivanovich Sechin and his friends.

16. Iraqi Oil Ministry- 2.3 million bpd

Iraqi Oil Ministry.

17. Qatar Petroleum- 2.3 million bpd

Qatar state oil and gas company, future global Gazprom. World leader in natural gas liquefaction projects.

18. Lukoil- 2.2 million b / d

General sponsor of the football team Spartak (Moscow).

19. Eni- 2.2 million b / d

A global Italian oil and gas company operating in dozens of countries around the world. It has a large network of gas stations under the Agip brand. The main distinguishing feature is the logo with a six-legged dog spewing fire. They say that the artist created it under the influence of the legend of the Nibelungs, but according to another version, completely different substances acted on him. Slightly more than 30% of the company's shares are directly and indirectly owned by the state, the rest is traded on stock exchanges. According to the law, no investor (except for the Italian state) has the right to concentrate more than 3% of the shares, do not even try.

20. Statoil- 2.1 million bpd

Norwegian oil and gas company, 2/3 of which is owned by the state. The basis of Norwegian socialism. The current main competitor of Gazprom in Europe.

21. ConocoPhillips- 2 mln b / d

American private corporation. In recent years, it has become famous for two controversial actions: the purchase and subsequent rapid sale of a large stake in Lukoil (up to 18%), as well as the spin-off and sale of an oil refining division. Now ConocoPhillips is arguably the world's only major upstream oil company.