The textile industry is the most important industry light industry, providing about half of the total volume of its production, and also occupying the first place in it in terms of the number of employees. Its main function is the production of consumer goods, primarily fabrics and knitwear. Along with this, it satisfies many production needs with its products. Depending on the raw materials used, the textile industry is usually divided into several subsectors - cotton, woolen, silk, linen, manufacturing fabrics from chemical fibers, as well as knitted and nonwoven fabrics.

Methods are mentioned such as combing, a clean woolen or semi-seam fabric, and sanding used on a coarser and cheaper material. Cleaning and siphoning was carried out several times, for example, the debris was removed from the scrapers, cuttings were cut out on the cut. Radiation has been used for long-haired fabrics such as winter coats, ladies' coats, faux fur, etc. the hot stamping of the goods brought the finishing shine and smoothness to the cut and the meticulously matte fabric.

By decapitation or steaming, the penetration of moisture into the woolen hair is avoided and thus dyes, for example after rain. This section is followed by a section on men's fashion during the First Republic. This chapter presents the following sections of the book. It was deliberately chosen to look at men's fashion, because in Brno the business focused mainly on male customers as carriers of coats, trousers, jackets, coasters and sportswear.

The textile industry is the oldest of all branches of the modern industry. It was with her that the industrial revolution in England began in the 18th century, marking the transition from manufacturing to factory production, which, after the invention of the steam engine, also led to the formation of the first large industrial areas... Then this path of capitalist industrialization was followed by other European countries, Russia, the United States, and some Asian countries. For a long time, the textile industry remained the leading industry in most developed countries of the world, but in the 20th century. its share in both gross output and employment of the economically active population began to decline, and in the second half of the same century it entered a period of prolonged structural crisis. As the countries of Asia, Africa and Latin America the relationship between the North (which in the 19th century, with the help of the export of its cheap factory textiles, contributed to the actual destruction of this industry in many colonial and semi-colonial countries, for example, India), and the South began to change.

The main topic of the presented book is acquaintance with the production of a number of selected companies of the first republic, which is an integral part of the book. The reader is familiar with the process of creating seasonal collections, selecting samples, references and materials. He also managed to record business correspondence between foreign intelligence agencies and Brno companies, which compared foreign market trends and competition opportunities with a paid service. On the basis of the preserved material of the collection from the Technical Museum in Brno, a list of companies containing samples of books or a sampler with attached textile samples was compiled.

The textile industry is not one of the dynamically developing sectors of the world economy. At least in the 90s. XX century world production fabrics of all types remained approximately at the level of 100–120 billion m 2 per year. The growth rate of the global consumption of textile fibers, which grew rather rapidly until the early 1990s, then slowed down (fig. 83). However, this does not mean at all that the industry has remained, as it were, in the "rain shadow" of the scientific and technological revolution. On the contrary, the scientific and technological revolution had a very large impact on it - primarily due to the automation and electronization of textile production, changes in its structure, nature of placement, etc. the last decades have had two factors. First, it is dramatic shifts in her raw material base and accordingly in its sectoral structure... Secondly, it is changing the role of individual orientation factors its location, which led to very significant shifts in its territorial structure.

Thanks to this, for the first time it became clear to demonstrate the company with its assortment. Grandsons of Auspice, Max Kon, sons of Moritz Beran, Moritz Fr. Samples of the companies' seasonal collections are commented on in the rich picture app. Fashion reports and descriptions of the wide range of woolen fabrics produced during the First Republic helped make woolen fabrics transparent and consistent. Due to the state of the stored samples and their quantity, but also with regard to the laboratory testing capabilities, it must be said that more and more new results and additional knowledge can still be expected.

Rice. 83. Dynamics of world production of textile fibers in 1950-2005

Let us first dwell on the characteristics of the raw material base of the textile industry. The main change in this area, closely related to the achievements of scientific and technological revolution, is a gradual but steady reducing the proportion of natural fibers and an increase in the proportion of chemical fibers, especially synthetic ones. This made it possible to significantly expand and strengthen the raw material base of the industry. How exactly the proportion between natural and chemical fibers changed is shown in table 117.

The publication is free of charge for scientific or scientific purposes, is not for sale, and should not be subject to sale. Additional Information on the site. The postage is borne by the applicant. Does this mean that this is a question for the textile industry? This gives rise to the logical negative impression that the textile industry is nowhere to be found and is still in ruins. However, there are five hundred and fifty operating textile and clothing companies with twenty or more employees. But companies with over 500 employees are no longer an exception.

Analysis of table 117 shows that by the mid-1990s. consumption of natural and man-made fibers has actually become equal. At the same time, the structure of consumption of natural fibers has changed quite little: as before, 80% of it is accounted for by cotton, 11% - by wool, and the rest - by other types of these fibers. The structure of consumption of chemical fibers, on the contrary, has changed very much in recent decades: for example, in 1955 the ratio of artificial (viscose) and synthetic fibers was in the ratio of 90:10, and in the middle of 2005 - 7:93.

Thus, in terms of employment, they cannot be compared to the remuneration of the Prostmiyevs. Despite the fact that the textile, textile and clothing industry is still in operation, it still employs sixty thousand people. How could such a large company as the Prostejovskaya Conciliation Firm collapse? Is there cheap competition from Asia? Cheaper competition is certainly the reason for this, but if that were the only reason, it would probably be a very long time for these problems.

From this point of view, the worst situation in the textile industry was about five years ago and in the termination of something earlier. So cheap competition, yes, but you have to add to it. Their determination is possible only after a deep analysis of all compounds. Generally speaking, companies with a “pre-revolutionary history” must deal with a certain size and structure, and historically their success has been a matter of employment. Maintaining these two values, especially in today's industry, has been an invaluable task.

Table 117

CHANGE OF THE WORLD STRUCTURE OF TEXTILE FIBER PRODUCTION IN 1950-2005

Another important structural and technological innovation of the scientific and technological revolution era is the rapid development of knitwear production, which in Western countries has become almost the main sub-industry of the entire textile industry, surpassing the production of fabrics in terms of production cost. This is largely due to the fact that labor productivity in knitwear production is several times higher than, for example, in weaving. But the industry of nonwovens, which are increasingly used for technical purposes, developed at an even faster pace. In addition, labor productivity in this sub-industry is even higher than in knitwear.

So how is the textile industry thriving today? What is changing is the content of the textile and revitalization business. We're starting to look more like the Dutch revolutionary industry, where you can find a factory with over ten parts, but the Dutch Revision Association has about nine hundred members.

So what should companies in Jews do? We must stop our success by using us first. This is evidenced by a number of our textile and clothing companies, whose business project is based on know-how, which is design, finance, markets, logistics and quality. In other words, they create a business brand and create a reliable person capable of providing it with reasonable quality and price. Such a business project can achieve big sales, but in the conditions of the European Union and their labor costs are hardly busy.

Changes in the raw material base of the industry have largely determined shifts in its sectoral structure. At the beginning of the XXI century. the world produced 92 million m 2 of cotton fabrics (on average 14 m 2 per capita), 21-22 million m 2 of silk fabrics (9 m 2 per capita), 2.5 million m 2 of woolen fabrics (0.5 m 2 per capita) and even less linen and other types of fabrics. As for chemical fibers, it should be borne in mind that they are now mainly used in the so-called mixed fabrics, that is, in combination with wool, silk, cotton (in particular, this applies to the most massive polyester fiber).

Of course, the question is immediately answered, which then provides employment. Over time, the bailiff paid the most for this. If this is not the case, circumstances will be foolish to tighten the noose around the neck. Was the size of the firm the main problem in the enterprise? Savvy company size is all about balancing flexibility — the ability to respond quickly to market demands — and the power of opportunity. Small businesses are generally flexible but vulnerable.

Large ones are relatively stable, but less flexible. Can firm flexibility be significant in today's firm? Yes, it cannot be automatically excluded. Ensuring flexibility in a large business must have its own internal processes. When the products of this group appeared on the market, some consumers believed that it was an American brand, and these products were very popular. In other words, the company built a new product group in which customers were willing to pay even “Czech” production costs.

For example, almost all production of silk fabrics these days is based on chemical fibers.

Changes in the geography of the global textile industry are also partly due to shifts in its raw material base, but they are even more dependent on factors such as cost work force... It turned out that in this respect the differences between economically developed and developing countries are truly enormous: for example, in Indonesia, the cost of labor is $ 0.24 per hour, in Pakistan - 0.4, in India and China - 0.6, and in USA - 13, in France - 14-15, in Germany - 21-22 dollars per hour. It was the cheapness of labor that played a decisive role in the “great migration” of the textile (and, let's add, clothing) industry from developed to developing countries, which has been taking place at least over the past three decades. It should be borne in mind that in India,

Permeated signs that at best, a smart workroom with three hundred people will function. What do you think about this? This is definitely a way to keep at least some of the production. The popularity of costumes is growing and can be financially interesting. And it probably can't be a question of how many people it is. It's only fifty workers or three hundred employees. Of course, as far as the previous employment is concerned, this is a significant drop and some people seem to be better off closing the plant.

However, there are hundreds of people. And in the industrial revolution, even in a European context, that would be big business. The only thing that can be said is that it is not easy. In the office of his small family business, Alessandro Barberis Kanonino explains what a distinguished European client called him and said that he was leaving China due to cost and demand for quality. That is why he needs the help of the people from Biella for his large collection.

Pakistan, Bangladesh, Syria, Turkey, Iran, Egypt, Morocco, Mexico, Colombia, Brazil, Argentina, this industry developed even before World War II and, therefore, needed significant modernization, and in the newly industrialized countries of Asia (for example, Thailand) it was formed relatively recently on a completely modern technical basis. In the 1990s. the process of reducing the production of fabrics (except for mixed fabrics) in developed countries and an increase in their production in developing countries continued especially actively. As a result, from 1970 to 1990, the countries of the South almost doubled their production on the world market and at the beginning of the XXI century. their share in the world production of fabrics has already reached 2/3.

Read about interesting textile work. But China is undoubtedly the leader in the textile industry. More than 4.6 million people are employed in the textile industry, according to the China Statistical Bureau, the Ministry of Industry and Information Technology and the China Chamber of Commerce. Nevertheless, wage growing annually at more than 12 percent, faster than the growth of the economy. For a long time, wages are not so low that the local industry can only compete with price.

At the same time, the Chinese textile industry is facing rising input costs such as cotton and wool, high import taxes on main production facilities and more expensive environmental regulations. The government's five-year plan for the textile industry, released last September, recognizes that higher costs have weakened China's international gains and that the sector faces a dual threat - from both developed countries like Italy with better technology and developing countries with better technology. lower wages.

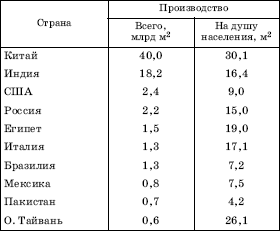

The same geographic shift can be traced to the example of individual subsectors of the textile industry, primarily the main one, cotton. To do this, it is enough to get acquainted with the top ten countries for the production of cotton fabrics. Developing countries, although they do not predominate in it quantitatively, far surpass the developed ones in terms of production (Table 118).

Read about the Chinese economy. This trend is quite clear - he added. Market proximity is also an advantage when Western clothing brands are under increased pressure to offer more collections, while consumers increasingly want clothing to quickly adapt to their desires. Suppliers need to be closer and faster. Quality and transparency are also important to customers.

While vendors are reluctant to name the brands they sell as part of their trade secrets, several international apparel companies are moving to the Italian wave to identify their source on their labels to differentiate themselves from the competition.

The same shift can be clearly seen in the production of fabrics from chemical fibers, but less so in the production of woolen and silk fabrics. It is important to add that the developing world also has its own differences. For example, the sub-regions of East and South-East Asia have now become a kind of epicenter of the world textile industry.

Table 118

Starting points for research

The textile and clothing industry is a sector that faces significant competition in world markets, especially with domestic raw materials, mainly from Asia.

Assessment of the development of the textile and clothing industry

All enterprises, but especially those that produce standard production, must include in their strategic intentions preparation for the growth of competitiveness and the changing conditions associated with entering the single market.An important step towards maintaining the competitiveness of the textile and apparel industry is to define their strategy for prioritizing and addressing the consequences of restructuring and modernization processes, that is, freeing workers in these processes.

TOP TEN COUNTRIES BY COTTON FABRIC PRODUCTION SIZE IN 2005

The main geographical shift described above is also associated with changes in foreign trade in textiles. Back in the mid-1980s. developing countries accounted for about 1/4 of the world's textile exports, but now their share is much larger. In many of these countries, the textile industry has a pronounced export orientation, so that 2/3 and even 3/4 of the goods it produces are sometimes sent to foreign markets. That is why China (together with Hong Kong) occupies the first place in the export of textiles in the world today (together with Hong Kong), and among the developed countries the group of leaders includes Italy, Germany, the USA, and the Republic of Korea.

Plans and measures to strengthen the competitiveness of the sector

Considering the market situation, product innovation and the introduction of new types of products with a higher share of added value, new functions and special focus, high quality with the appropriate service are top priority. Such products may emerge in the near future by linking manufacturers with R&D bases, universities, supplier networks, and customers from related industries or business networks. This process has already been implemented in the Czech Republic through the creation of associations or clusters.

Russian textile industry in the 1990s was in a state of deepest crisis: in the first half of that decade alone, its production decreased by 80%. As a result, the share of the textile industry in the country's GDP decreased over the same period from almost 8% to less than 2%, and in the revenue side of the budget - from 26 to 2%. Such a sharp drop in production was caused by a number of reasons, including the loss of all traditional sources of cotton and wool supply, the residual principle of financing, a low technical level and an ineffective production and organizational structure, which is characterized by many large enterprises (employing more than 1000 people), which does not allow flexible and quick response to market demands. Only in the late 1990s. this decline has been halted, so there is hope for a revival of the country's oldest industry.

Many clusters abroad are also successful in the textile and clothing industry. The main priority was the creation of an experimental cluster in the textile and apparel industry. It continues with an analysis of the current value chain of the textile and apparel industry in the Czech Republic in order to determine its composition and determine the share of individual items in the value chain. The family-owned company produces everything in Sumperk in northern Moravia. The difference in the cost of wages between them plays only a minor role.

- a branch of the economy, which includes enterprises for the manufacture of fabrics, garment production, as well as the production of leather and leather goods. These are the three main branches of light industry, which in turn are divided into smaller subsectors. The volume of shipped goods produced by light industry enterprises in Russia in 2014 amounted to 289.7 billion rubles. Of these, about 44% fell on the sewing industry.

Compared to 2013, there was a drop in production in all sectors of the light industry. The production index in the clothing industry and the textile industry for 2014 was 97.5, and in the production of leather, footwear and leather goods, this indicator is 97.2. According to production indices, light industry takes 11th and 12th places out of 14 main types of manufacturing industries. In monetary terms, the volume of shipped products compared to 2013 decreased by 2.1%, while the production of fabrics and clothing production remained at the level of 2013, and the decrease in shipments in the leather industry amounted to 11.8%.

To support the light industry in 2014, 1.7 billion rubles were allocated from the federal budget, and in 2015 the government plans to spend another 1.5 billion on the development of the industry. But, despite these measures, the Russian light industry provides only about 25% of the domestic market, the remaining 75% are exported. By far the most developed light industry has China. At the end of 2014, about 32% of all products of the global light industry were produced in China. Also among the world leaders in light industry are the countries of South Asia, such as Indonesia, India, Pakistan, Bangladesh. Country Western Europe and the USA also have a developed light industry, but their main focus is the production of clothing and footwear of famous world brands from raw materials obtained from developing countries. European leader for the production of light industry goods is Italy, where a large number of trading houses are concentrated, specializing in the production of clothing, footwear and leather goods.

The light industry of the Russian Federation employs almost 330 thousand people. At the same time, about 1/3 of employees work in small enterprises with less than 50 employees. In total, there are about 3.2 thousand small enterprises operating in the light industry in Russia. At the end of 2014, their turnover amounted to 22.3% of the total production of the Russian light industry, which in monetary terms is equal to 64.44 billion rubles.

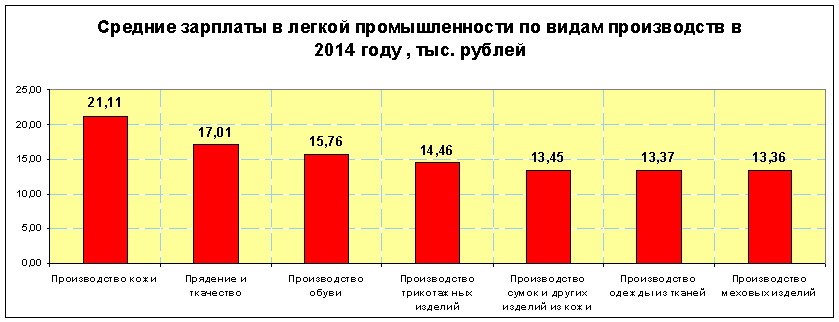

The wages in the industry remain one of the lowest in Russia. In 2014, the average wages of workers in the textile industry and clothing industry amounted to 14 468 rubles, and workers in the leather and shoe production 16 053. Thus, the wages by industry are lower than the average in Russia by 55% and 50%, respectively. The highest average wage for workers employed in leather production is 21,106 rubles, and the smallest for workers employed in fur production is 13,365 rubles.

One of the reasons for such low wages in the industry is the high share of shadow business in production, as well as the sale of counterfeit products of foreign and domestic production. For example, the share of shadow imports of footwear to Russia in 2014 amounted to 66.4% of all imported footwear. In footwear sales, shadow imports account for 57% of all products sold. About 35% of all footwear and clothing in Russia is sold in markets where individual entrepreneurs trade. Unfortunately, most of the products sold are either foreign counterfeit products or products manufactured in Russia in illegal workshops. All this significantly hinders the development of light industry at the all-Russian level, although for some regions light industry enterprises are city-forming. This is especially true of the Ivanovo region of the Russian Federation, where the share of light industry in the total volume of production is 33%.

Textile industry

The textile industry is a branch of light industry, which is the basis of the light industry. Textile production is understood as the production of yarn, threads, fabrics based on fibers of plant, animal and artificial origin. The textile industry includes the following subsectors:

- Production of cotton fabrics;

- Production of woolen fabrics;

- Production of linen fabrics;

- Silk fabric production;

- Manufacture of fabrics from artificial fibers;

- Production of nonwovens.

The products of the textile industry serve as raw materials for other industries of the light industry, and are also used in the manufacture of consumer goods, this primarily applies to nonwovens.

Nonwovens are textile fabrics that are created without the use of weaving technology. That is, the threads are not intertwined, but gluing, needling, felting, knitting are used to fasten them. These materials are further used for the manufacture of shoes and outerwear, nonwovens made using paper machines are used for the manufacture of napkins, tablecloths and bed linen. The most widespread are glued nonwoven materials, they are used as a base for polymer coatings, as well as container, wiping, filtering and soundproof materials.

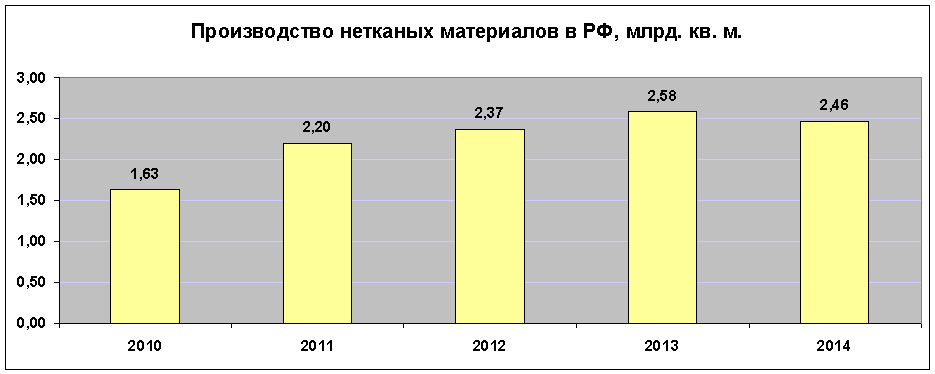

The production of nonwovens in Russia at the end of 2014 amounted to 2.461 billion square meters. meters. This accounts for just over 1% of world production. In total, about 201 billion square meters were produced in the world over the past year. m. of nonwovens, which is approximately 7.9 million tons. The leaders in the production of these products are the EU countries, the USA and China.

If we consider the production of fabrics in Russia with the use of weaving equipment, then the bulk of the fabrics produced is cotton. In the structure of the world textile industry, cotton fabrics account for 67% of total production, in Russia this figure is 82.7%. In total, in 2014, 1.187 billion square meters were produced in the Russian Federation. m. cotton fabrics. This is 10% less compared to 2013.

In general, 2014 was marked by a significant drop in the production of fabrics from natural raw materials. Thus, the decline in the production of woolen fabrics was 11.2% and amounted to 11.5 million square meters. meters, and the production of linen fabrics fell by 16.8% to 31.4 million square meters. m. In the Ministry of Industry this is explained by the lack of raw materials for the textile industry. But also do not forget that the cost of producing domestic textile products is higher than imported ones, which in turn affects production volumes. So the production of woolen fabrics in the Russian Federation, compared to 2010, has been reduced by almost half.

Slightly better is the situation with the production of fabrics from artificial fibers, as well as natural silk fabrics. Production of fabrics from man-made fibers in 2014 decreased by only 1% and amounted to 207 million square meters. m. And the production of natural silk fabrics compared to 2013 increased by 21% to 192 thousand square meters. m.

clothing industry

On average, in Russia, spending on non-food products is 37% of the total. At the same time, the share of garment products accounts for about 8% of Russians' expenses. Physical clothing made of fabrics after an increase in production in 2013 by 5.8% in 2014 decreased by 0.4%. As for the shipment of goods from the garment industry, in monetary terms, an increase of 5.8% is observed. According to this indicator, growth has been taking place over the past three years. In 2014, the largest growth in the garment production was shown by the North-West Federal district- 52.7%, in turn, a significant decrease in volumes was recorded in the Southern Federal District - 33.5%. For the Federal Districts of Russia, the structure of garment production shipments is as follows:

- Central Federal District - 42.4 billion rubles. Share in total shipments - 33.1%

- Northwestern Federal District - 36.3 billion rubles. Share in shipments - 28.4%

- Volga Federal District - 18.9 billion rubles. Share in shipments - 14.8%

- Southern Federal District - 17.7 billion rubles. Share in shipments - 13.8%

- Siberian Federal District - 6.2 billion rubles. Share in shipments - 4.8%

- Ural Federal District - 3.9 billion rubles. Share in shipments - 3%

- North Caucasian Federal District - 1.9 billion rubles. Share in shipments 1.5%

- Far Eastern Federal District - 0.7 billion rubles. Share in shipments 0.5%

The financial situation in the garment industry is much better than in the textile industry. At the end of 2014, garment enterprises accounted for an average of 17%, while in the textile industry this figure is 2.8%. But, despite good financial performance, the share of imports in the industry continues to grow. In 2014, due to the adopted restrictions on the supply of goods to The Russian Federation, legal imports of clothing decreased by 5.5% and amounted to USD 7.74 billion. But at the same time, shadow imports have increased. This confirms the fact that the volume of production in 2014 decreased by 0.4%, legal imports decreased by 5.5%, and sales at the same time, compared to 2013, increased by 2.5% (in this case, we mean total sales in the domestic market, and not just sales of goods from Russian manufacturers). Thus, we can confidently assert that shadow imports continue to grow, filling the market share of legal imports and goods from Russian manufacturers.

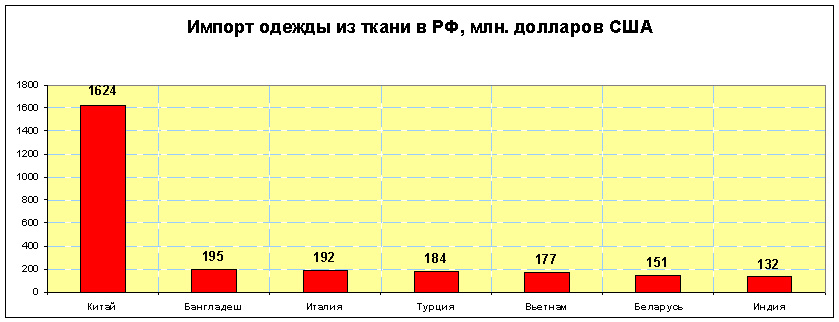

China is the largest clothing importer to the Russian Federation. The share of imports of Chinese clothing made of fabrics is about 48% of the total. The top five also include Bangladesh, Vietnam, Turkey and Italy.

The main directions in the sewing industry are the production of coats and short coats, jackets, suits, dresses and sundresses, trousers and shorts, as well as sewing overalls.

In 2014, Russian light industry enterprises produced 1,239 thousand coats and short coats. This is the only type of clothing for which there has been a decline in production. In 2013, the Russian light industry produced 1,335 thousand pieces, and in 2012 - 1,469 thousand pieces. Thus, a sufficient stock was formed in the warehouses, which led to a decrease in production volumes.

The bulk of the produced coats and short coats are female models; in 2014, 1,019 thousand pieces of them were sewn, which is 82.2% of the total. 220 thousand pieces of men's coats and short coats were produced. The largest companies producing this type of outerwear in the Russian Federation at the end of 2014:

- OJSC "Mayak" (Nizhny Novgorod Region) - 81,600 pcs.

- LLC "Sinar" ( Novosibirsk region) - 68 600 pcs.

- Baltic Line CJSC (Kaliningrad Region) - 57,300 pcs.

- CJSC "Elegant" (Rostov region) - 46 600 pcs.

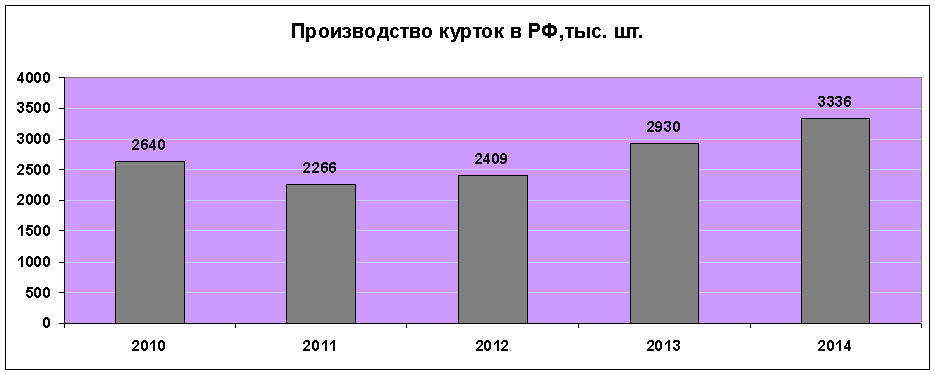

Unlike the production of coats and short coats, the production of jackets Russian enterprises light industry has been growing steadily over the past three years. So in 2014 the increase in production was 12.2%.

In 2014, 3,336 thousand jackets were sewn, of which 2,034 thousand were for men and 1 302 thousand for women. Compared to 2013, the production of jackets for men increased by 392 thousand pieces, and for women - by 239 thousand pieces. The largest Russian manufacturer of jackets is CJSC Gloria Jeans, which is located in the Rostov region. Its share in the volume of production of this type of clothing is just over 40%. In 2014, this company produced 1 348 thousand jackets. Other large companies for sewing jackets in the Russian Federation:

- LLC "Vitekskom" (Moscow region) - 64,100 pcs.

- LLC Ariadna-96 (Rostov Region) - 32,300 pcs.

- OJSC "Kukmorskaya sewing factory" (Tatarstan) - 24,500 pcs.

Suits production increased by 13.8% in 2014. This is the largest increase among all major types of clothing. Such an increase is associated with the fact that the warehouses of enterprises had small balances of goods - at the beginning of the year, about 10% of the shipment of these enterprises.

The bulk of the suits produced are for men, about 90% of all made. In 2014, Russian enterprises manufactured 5,264,000 suits, of which 4,735,000 were for men. The largest Russian costume manufacturers:

- JSC Pskov sewing factory "Slavyanka" - 330,800 pcs.

- JSC Sudar (Vladimir region) - 183,000 pcs.

- JSC "Elegant" (Ulyanovsk region) - 124,100 pcs.

- OJSC Peplos ( Chelyabinsk region) - 106 700 pcs.

The production of dresses and sundresses has more than doubled over the past 5 years. In 2014, 8,867 thousand units were produced. dresses and sundresses. This is 10% more than in 2013. The production of dresses and sundresses is very concentrated and although they are produced in all Federal districts, at the end of 2014 - 73% was produced in the Southern Federal District, and 12.3% - in the Central.

![]()

The main manufacturer of dresses and sundresses in Russia is CJSC Gloria Jeans Corporation. It accounted for about 68% of the total Russian production, which in quantitative terms is 6 008 thousand pieces. Other large companies for the production of dresses and sundresses in Russia:

- CJSC PKF "Elegant" (Rostov region) - 171,500 pcs.

- CJSC Vyaznikovskaya sewing factory (Vladimir region) - 81,100 pcs.

- LLC "KP Manufactures" (Moscow region) - 53,800 pcs.

The production of trousers, breeches and shorts is the most massive. In 2014, 21.4 million units were produced. of this product. Compared to 2013, the increase was 400 thousand units. The share of men's trousers accounts for 42.3% of the total production, the remaining 57.7% is the production of women's trousers, shorts and breeches. Largest manufacturer of this product in Russia - JSC "Corporation Gloria Jeans". At the end of 2014, this company produced 15,548 thousand trousers, shorts and breeches. Other major Russian companies for the production of this type of clothing:

- CJSC Peplos (Chelyabinsk Region) - 136,300 pcs.

- JSC Pskov sewing factory "Slavyanka" - 135 800 pcs.

- JSC "Alexandria" ( Krasnodar region) - 99 300 pcs.

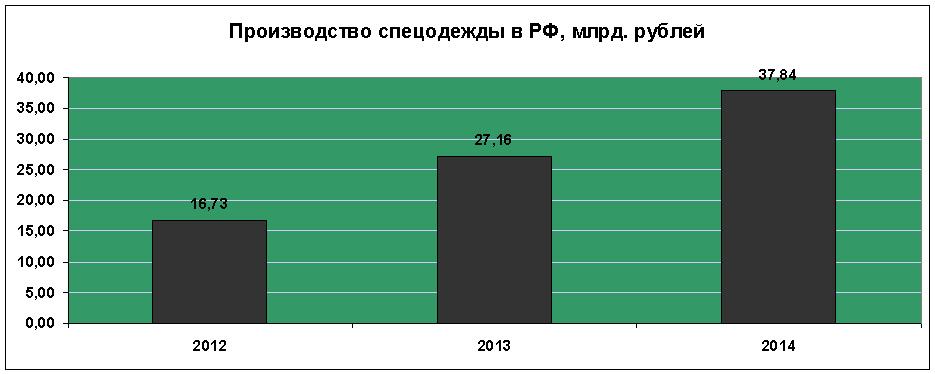

The production of workwear occupies an important place in the sewing industry, because in addition to the constantly growing demand for products, a significant part of it is sewn in correctional institutions and enterprises of disabled people's societies, thereby providing jobs for these categories of citizens. In total, in 2014, about 112 million pieces of workwear were produced. That is 6 million more than in 2013. The total production volume amounted to 37.84 billion rubles.

In addition to the main types of clothing listed above, the Russian light industry in 2014 produced:

- Windbreakers and similar products - 769,000 pcs.

- Skirts and skirt-trousers - 4,476,000 pcs.

- Shirts for men and women blouses and body shirts (except for knitted shirts) - 4,864,000 pcs.

- Women's coats and short coats made of natural fur - 108 270 pcs.

Manufacture of leather and leather products

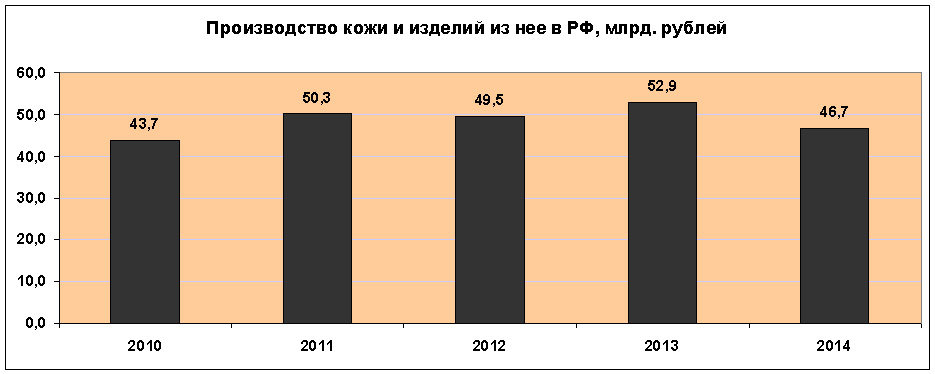

The turnover in the leather industry is significantly inferior to the total turnover in the clothing industry and the textile industry. In 2014, the revenue of enterprises in this industry of the light industry amounted to 46.7 billion rubles. This is the worst indicator in the last three years. At the same time, the industry's enterprises have a rather low profitability - 6.9%. And the overall balanced result of enterprises in this branch of light industry has a negative indicator for the second year in a row. In 2014, the financial sector in the industry was equal to (- 824) million rubles.

This branch of the Russian light industry includes three main areas: leather production, footwear production and leather goods production.

Leather production is one of the few branches of the Russian light industry in which exports exceed imports. Leather production in Russia has been declining since 2010. Compared to the previous year, production decreased by 4.2% and amounted to 2,199.2 million sq. dm. In the general structure of production, the main share is made up of chrome leather goods, that is, leather tanned with the help of chromium compounds. The production of hard and soft (yuft) leather is ten times less.

In the Russian Federation, leather is produced at 22 two enterprises, and 20 of them produce chrome leather goods. In addition, 7 enterprises have capacities for the production of yuft leather and 5 for the production of hard leather. Each industry has one that produces more than 40% of the total volume in the country:

- Chrome leather - CJSC “Russian leather” (Ryazan region) - 1012.7 million sq. Dm. (47.2% of the total).

- Yuft leather - Vakhrushi-Yuft LLC (Kirov region) - 20.1 mln. Sq. M. dm. (55.5% of the total).

- Hard leather - Chevro LLC ( Voronezh region) - 9.8 million sq. dm. (51.5% of the total).

The main part of leather production is located in the Central Federal District, which accounts for 72.7% of chrome leather production and 9.4% of yuft leather goods. The second place is occupied by the Volga Federal District with indicators of 18.7% and 61.3%, respectively. On the third line is the Southern Federal District, where the production of chrome leather is 6% of the total, and yuft leather - 26.2%. The share of other Federal Districts in this light industry is insignificant.

The production of leather is significantly influenced by the number of imports and exports of products. So in 2013, exports accounted for 28.3% of the production volume, and imports - 36.1%. And in 2014, the indicators changed dramatically - exports amounted to 48.7%, while imports fell to 27%.

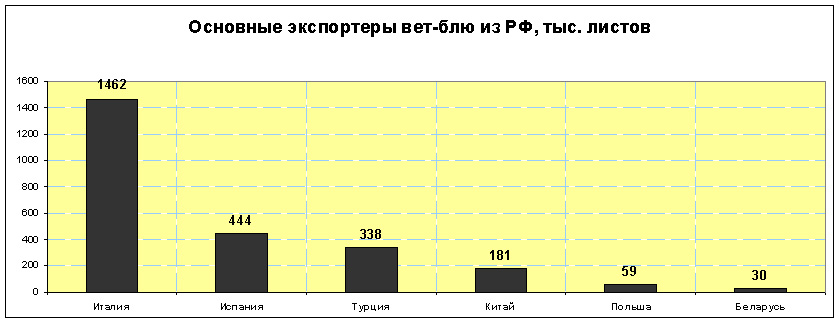

The main Russian export items are cattle wet-blue and crust, as well as finished leather. Wet blue is a type of tanned leather that is not completely dried, while crust is a leather without a top finish that retains its natural pattern. Wet blue is sold in standard sheets, and Italy is the main buyer of this product in Russia.

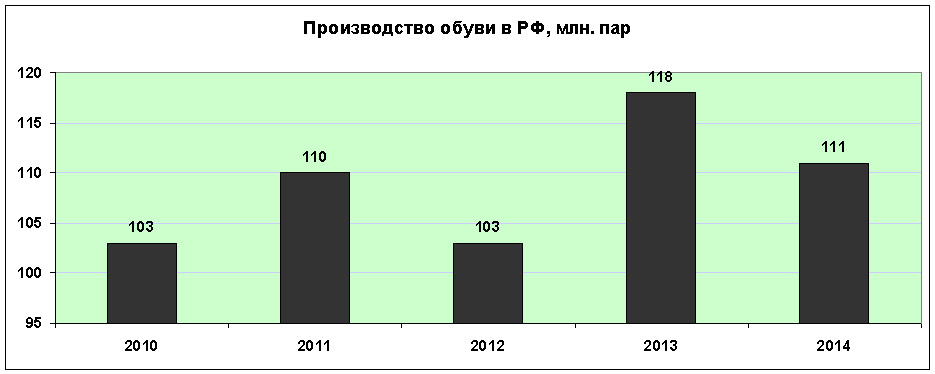

In 2014, footwear production in the Russian Federation decreased by 6% and amounted to 111 million pairs. Of these, shoes with leather and textile tops account for 60.8 million pairs, and rubber and plastic shoes - 41.6 million pairs. 2.8 million pairs of sports shoes and 5.8 million pairs of safety and other footwear were produced.

Although the factories for the production of footwear are located in 7 Federal Districts, the main volume of production falls on the Central. At the end of 2014, 45.34% of all footwear was produced at the enterprises of this district. The output of footwear with leather and textile tops in the districts of the Russian Federation is as follows:

- Central Federal District - 27.57 million pairs;

- Southern Federal District - 14.71 million pairs;

- Volga Federal District - 11.67 million pairs;

- Siberian Federal District - 2.23 million pairs;

- Ural Federal District - 2.21 million pairs;

- North Caucasian Federal District - 1.58 million pairs;

- Northwestern Federal District - 0.89 million pairs.

As in other branches of light industry, there is a pronounced leader in the shoe industry in Russia. Bris-Bosfor LLC (Krasnodar Territory) produces 31% of all footwear with leather and textile tops in Russia, which in quantitative terms amounts to 18.8 million pairs. Other major companies in this industry:

- LLC MuyaProduction (Vladimir region) - 3.44 million pairs;

- Unichel Shoe Firm CJSC (Chelyabinsk Region) - 2.98 million pairs;

- Ralph Ringer CJSC (Moscow) - 1.62 million pairs;

- JSC "Torzhok shoe factory" (Tver region) - 1.47 million pairs.

Russian footwear exports are much less than imports. At the end of 2014, 5.65 million pairs were exported for a total amount of USD 122.4 million. The main buyers of Russian footwear are the CIS countries.

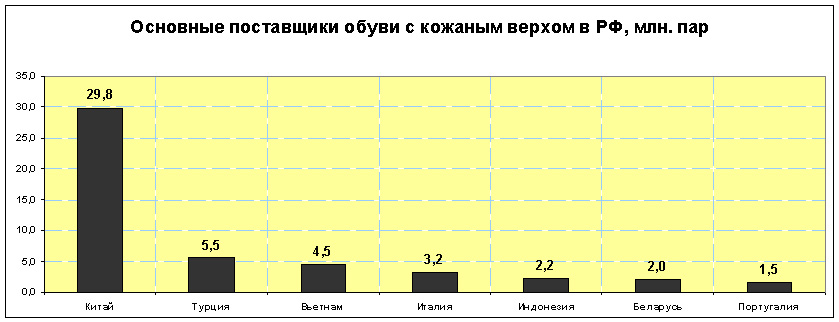

During the same period, 118.23 million pairs of shoes were imported to Russia for the amount of USD 2,281 million. The excess of imports over exports in quantitative terms was 21 times, and in monetary terms - 18.7 times. This once again confirms the fact that cheaper shoes are imported to the Russian Federation than Russian-made shoes. China is the main supplier of footwear to Russia.

The output of leather goods in the Russian Federation in 2014 decreased by 18.1% and amounted to 15,482 thousand items. Such a drop is primarily associated with a large amount of balances in the warehouses of enterprises, as well as a drop in demand for domestic products of this type. The largest decline in the production of leather goods was recorded in the Northwestern and Central Federal Districts, by 50.3 and 11.5%, respectively. In the city of St. Petersburg, the main center of the leather goods industry in the Russian Federation, production decreased by 51.2%, but in monetary terms, the profit decreased by only 17%. Companies with the largest production of leather goods (bags, folders, suitcases, etc.) at the end of 2014 in Russia:

- LLC "Logistic Inform" (St. Petersburg) - 2 684 thousand units.

- LLC Vladimirskaya leather haberdashery factory - 2,479 thousand units.

- CJSC "Medvedkovo" (Moscow) - 633 thousand units.

- CJSC Piterbag (St. Petersburg) - 292 thousand units.